KPI — October: State of the Manufacturing Sector

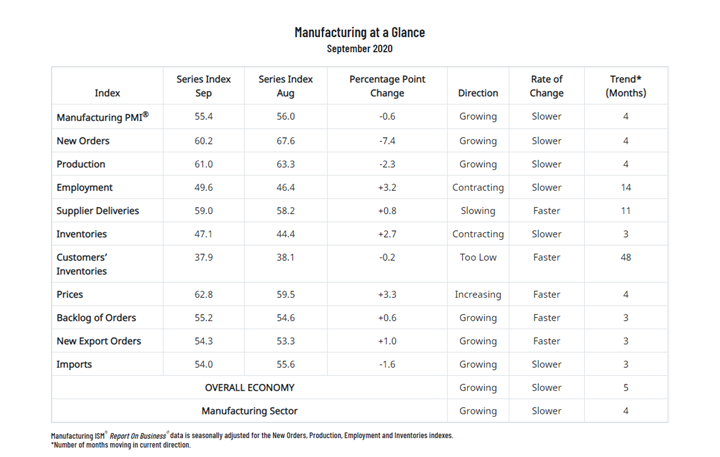

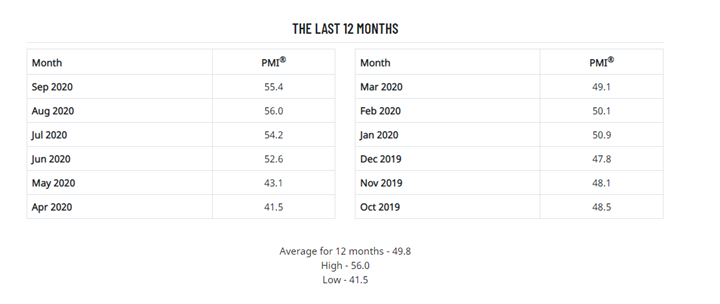

Economic activity in the manufacturing sector grew during September, with the overall economy securing a fifth consecutive month of growth, according to the nation’s supply executives in the latest Manufacturing ISM® Report On Business®. The September PMI® registered 55.4%, down 0.6 percentage point from the August reading of 56%.

The Report On Business® measures its data using the Purchasing Manager’s Index (PMI), which is an indicator of economic health in the manufacturing sector. A reading above 50% indicates that the manufacturing economy is generally expanding, while below 50% indicates that it is generally contracting. All data and analysis are courtesy of Institute for Supply Management.

“After the coronavirus (COVID-19) pandemic brought manufacturing activity to historic lows, the sector continued its recovery in September. Survey Committee members reported that their companies and suppliers continue to operate in reconfigured factories and are becoming more proficient at maintaining output,” said Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Furthermore, “Manufacturing performed well in the month with demand, consumption and inputs registering growth indicative of a normal expansion cycle. While certain industry sectors are experiencing difficulties that will continue in the near term, the manufacturing community as a whole has learned to conduct business effectively and deal with the variables imposed by the COVID-19 pandemic,” said Fiore.

- Demand expanded, with the (1) New Orders Index growing at strong levels, supported by the New Export Orders Index expanding moderately, (2) Customers’ Inventories Index at its lowest figure since June 2010, a level considered a positive for future production and the (3) Backlog of Orders Index expanding at a faster rate compared to the prior two months.

- Consumption (measured by the Production and Employment indexes) contributed positively (a combined 0.9-percentage point increase) to the PMI® calculation, with five of the top six industries continuing to expand output strongly. Additionally, employment neared expansion territory for the first time since July 2019.

- Inputs—expressed as supplier deliveries, inventories and imports—continued to indicate input-driven constraints to further production expansion, but at slower rates compared to August. Inventory levels contracted again due to strong production output and supplier delivery difficulties. Overall, inputs improved compared to August and contributed positively to the PMI® calculation.

Fourteen of the 18 manufacturing industries reported growth in September: Paper Products; Wood Products; Food, Beverage & Tobacco Products; Furniture & Related Products; Electrical Equipment, Appliances & Components; Nonmetallic Mineral Products; Fabricated Metal Products; Chemical Products; Miscellaneous Manufacturing; Plastics & Rubber Products; Machinery; Textile Mills; Computer & Electronic Products; and Transportation Equipment. The four industries reporting contraction in September are: Apparel, Leather & Allied Products; Printing & Related Support Activities; Petroleum & Coal Products; and Primary Metals.

Commodities Up in Price: Aluminum (4); Aluminum Extrusions; Copper (4); Freight (2); High-Density Polyethylene (HDPE) (3); Lumber (3); Natural Gas (2); Polypropylene (3); Polyvinyl Chloride; Precious Metals (3); Propylene (2); Resins; Sanitizers; Steel (2); Steel—Cold Rolled; Steel—Hot Rolled; Steel—Scrap (2); and Steel Products.

Commodities Down in Price: Oil

Commodities in Short Supply: Aluminum; Cable Assemblies; Capacitors; Lumber (2); Personal Protective Equipment (PPE); PPE—Gloves (7); PPE—Masks; Polypropylene; Resins; Resistors; and Sanitizers.

Note: The number of consecutive months the commodity is listed is indicated after each item. *Indicates both up and down in price.

What Respondents Are Saying

- “Still struggling with long lead times for components coming from China [contract manufacturers].” (Computer & Electronic Products)

- “Volume remains lower than one year ago but has steadily improved over the past two periods.” (Chemical Products)

- “Business is booming, and the supply chain has been caught off guard. We are working closely with our suppliers to ensure supply and try to control costs. The resin industry, along with plastics, is driving cost increases and scarce availability.” (Transportation Equipment)

- “Our business has not begun to recover.” (Petroleum & Coal Products)

- “Overall business conditions are improving, but not at the rates we saw them decline.” (Fabricated Metal Products)

- “Our customer order intake is increasing significantly for deliveries in the first half of 2021. Outlook is generally positive.” (Machinery)

- “Retail sales remain strong, but food service is still down about 15% year-over-year. All of our factories are still struggling with manning shifts due to positive COVID-19 cases and/or quarantine because employees came in contact with someone who contracted the virus.” (Food, Beverage & Tobacco Products)

- “Demand remains high, strong finish to 2020 projected, with an even stronger 2021 fiscal year. Prices have increased in certain categories, but no major price increases of our own have been implemented yet. We are seeing an uptick in reshoring opportunities in the third quarter across various industries and products.” (Electrical Equipment, Appliances & Components)

- “We are seeing a marked increase in international demand in Q4 compared to Q2 and Q3. Still not at historical levels; however, a positive outlook.” (Paper Products)

- “Raw material shortages, especially of hardwood logs, are starting to impact overall supply. Domestic market demand is fragmented but remains sound. Export demand, especially to China, is robust.” (Wood Products)

- “Business has continued to be strong, with September following August. October is also shaping up to be a good sales month as well.” (Plastics & Rubber Products)

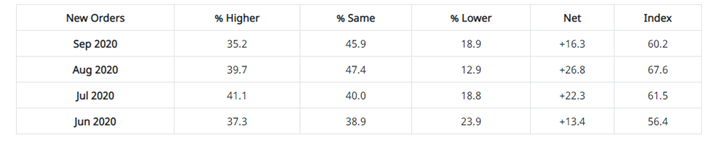

ISM®’s New Orders Index registered 60.2% in September, a decrease of 7.4 percentage points compared to the 67.6% reported in August. This indicates that new orders grew for the fourth consecutive month. “Four of the top six industry sectors (Food, Beverage & Tobacco Products; Fabricated Metal Products; Chemical Products; and Transportation Equipment) expanded,” explained Fiore. A New Orders Index above 52.5%, over time, is generally consistent with an increase in the Census Bureau’s series on manufacturing orders (in constant 2000 dollars).

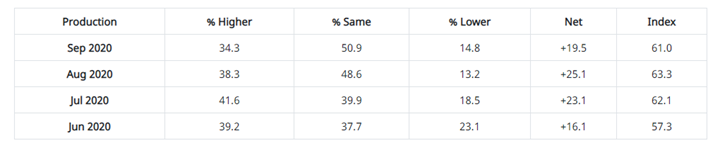

The Production Index registered 61% in September, 2.3 percentage points lower than the August reading of 63.3%, indicating growth for the fourth consecutive month. “Five of the top six industries (Chemical Products; Fabricated Metal Products; Transportation Equipment; Food, Beverage & Tobacco Products; and Computer & Electronic Products) expanded strongly,” added Fiore. An index above 51.7%, over time, is generally consistent with an increase in the Federal Reserve Board’s Industrial Production figures.

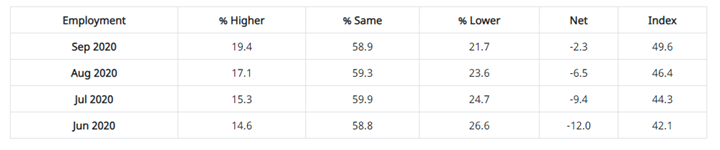

ISM®’s Employment Index registered 49.6% in September, 3.2 percentage points higher than the August reading of 46.4%. “This is the 14th consecutive month of employment contraction, at a slower rate compared to August. This marks the fifth consecutive month of improvement since the index’s low of 27.5% registered in April. Four of the six big industry sectors, (Computer & Electronic Products; Food, Beverage & Tobacco Products; Chemical Products; and Transportation Equipment) experienced expansion. Slowing inventories contraction typically indicates a need for more labor to maintain production output. Long-term labor market growth remains uncertain, but strong new-order levels and an expanding backlog signify potential employment strength for the fourth quarter. Survey panelists’ comments indicate that there are significantly more companies hiring or attempting to hire than those that are reducing labor forces,” said Fiore. An Employment Index above 50.8%, over time, is generally consistent with an increase in the Bureau of Labor Statistics (BLS) data on manufacturing employment.

The delivery performance of suppliers to manufacturing organizations was slower in September, as the Supplier Deliveries Index registered 59%. This is 0.8 percentage point higher than the 58.2% reported in August. “Suppliers continue to struggle to deliver, with deliveries slowing at a faster rate compared to August. Transportation challenges and continuing difficulties in supplier labor markets are still constraints to production growth. The Supplier Deliveries Index reflects the difficulties suppliers continue to experience due to COVID-19 impacts. These issues are not expected to diminish soon and, at this time, represent a continuing hurdle to production output and inventories growth,” said Fiore. A reading below 50% indicates faster deliveries, while a reading above 50% indicates slower deliveries.

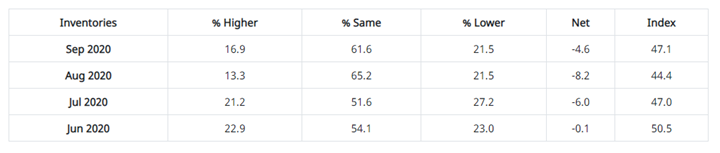

The Inventories Index registered 47.1% in September, 2.7 percentage points higher than the 44.4% reported for August. Inventories contracted for the third straight month, but at a slower rate. “Inventory levels remained in contraction due to continued strength in production and ongoing supplier difficulties,” explained Fiore. An Inventories Index greater than 44.3%, over time, is generally consistent with expansion in the Bureau of Economic Analysis (BEA) figures on overall manufacturing inventories (in chained 2000 dollars).

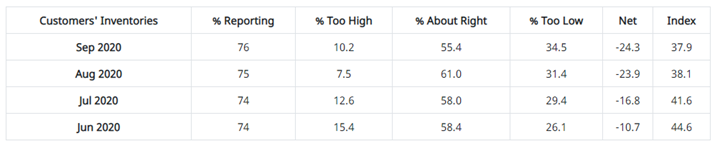

ISM®’s Customers’ Inventories Index registered 37.9% in September, 0.2 percentage point lower than the 38.1% reported for August, indicating that customers’ inventory levels were considered too low. “Customers’ inventories are too low for the 48th consecutive month and moved further into ‘too low’ territory in September, a positive for future production growth. It’s been more than a decade (a reading of 35.8% in June 2010) since the Customers’ Inventories index has been at this level,” said Fiore.

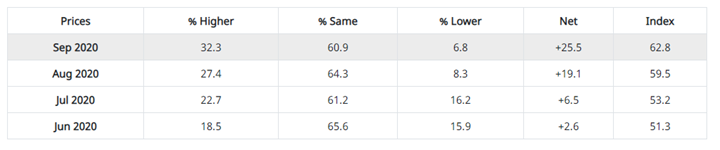

The ISM® Prices Index registered 62.8%, an increase of 3.3 percentage points compared the August reading of 59.5%, indicating raw materials prices increased for the fourth consecutive month. A Prices Index above 52.5%, over time, is generally consistent with an increase in the Bureau of Labor Statistics (BLS) Producer Price Index for Intermediate Materials.

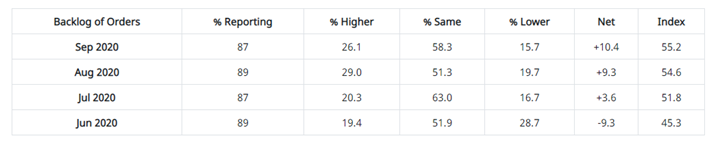

ISM®’s Backlog of Orders Index registered 55.2% in September, a 0.6-percentage point increase compared to the 54.6% reported in August, indicating order backlogs expanded for the third consecutive month after four straight months of contraction. “Backlogs expanded at faster rates in September, indicating that new-order intakes were sufficient to fully offset production outputs. Four of the six big industry sectors’ backlogs expanded (Fabricated Metal Products; Chemical Products; Food, Beverage & Tobacco Products; and Transportation Equipment). The index achieved its highest level of expansion since November 2018 (56.4%),” said Fiore.

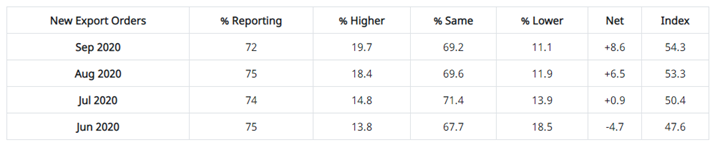

ISM®’s New Export Orders Index registered 54.3% in September, up one percentage point compared to the August reading of 53.3%. “The New Export Orders Index grew for the third consecutive month at a faster rate and reached its highest level since September 2018 (56%). With five of the six big industry sectors expanding, (Food, Beverage & Tobacco Products; Transportation Equipment; Fabricated Metal Products; Computer & Electronic Products; and Chemical Products), new export orders were a positive factor to the growth in new orders,” said Fiore.

ISM®’s Imports Index registered 54% in September, down 1.6 percentage points compared to the 55.6% reported for August. “Imports expanded for the third consecutive month, reflecting continued increases in U.S. factory demand,” said Fiore.

KPI — October: Consumer Trends

Key Performance Indicators Report — October 2020