KPI — November: The Brief

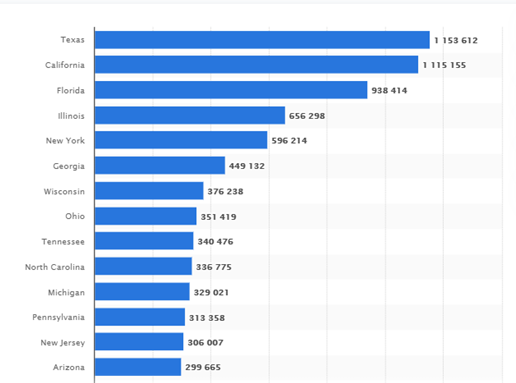

More than 12 million COVID-19 cases have been reported across the United States as of Nov. 23, with Texas, California, Florida and Illinois reporting the highest numbers, according to Statista.

Global markets are reacting positively to recent news that two COVID-19 vaccines are showing more than 90% effectiveness in late-stage trials; however, economic impacts due to the pandemic remain widespread, with tens of millions left unemployed to face new challenges.

In fact, a United Nations Conference on Trade and Development (UNCTAD) report published on Nov. 19 warns that a viable vaccine will not halt the spread of [global] economic damage; rather, it will be felt long into the future, especially by the poorest and most vulnerable.

The report, Impact of the COVID-19 Pandemic on Trade and Development: Transitioning to a New Normal, “provides a comprehensive assessment of the economic knock-ons, projecting that the global economy will contract by a staggering 4.3% in 2020 and warning that the crisis could send an additional 130 million people into extreme poverty.”

Real economic growth (U.S.) will increase by 2.2%* (annualized rate) in the fourth quarter of 2020, according to The Conference Board. The deceleration in recovery follows a contraction of 5% in Q1, a contraction of 31.4% in Q2 and a rebound of 33.1% in Q3. For context, the U.S. economy was still 3.5% smaller in Q3 of 2020 compared to Q4 of 2019, explained the Bureau of Economic Analysis (BEA).

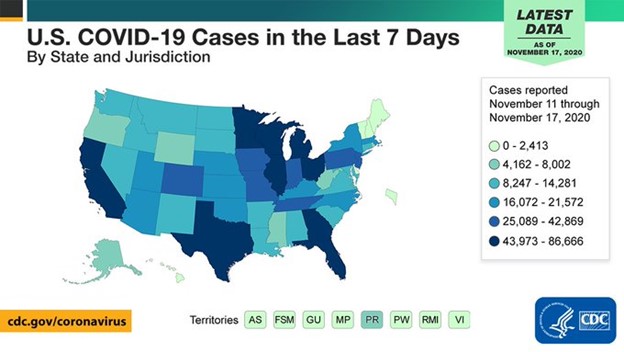

According to the Centers for Disease Control and Prevention (CDC), COVID-19 cases are rising. “Average daily cases are up 43% compared to the previous seven days, with 94% of U.S. jurisdictions seeing more cases. This Thanksgiving, help slow the spread: gather outdoors, wear a mask, stay six feet apart.”

Certainly, more hard times are ahead as global markets work toward recovery, but the American story is a standout. “Despite facing challenges at the domestic level along with a rapidly transforming global landscape, the U.S. economy is still the largest and most important in the world, representing about 20% of total global output,” according to FocusEconomics, a leading provider of economic analysis and forecasts for 131 countries.

While many small businesses across the country are struggling, professionals across the automotive aftermarket, powersports and RV industries—to name a few—are turning to new and improved ways to engage with customers, evolve their business models and grow their brands.

As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and automotive industry to current economic conditions and consumer trends.

For starters, total nonfarm payroll employment rose by 638,000 in October, with the unemployment rate declining to 6.9%. Furthermore, nonfarm payroll employment increased in 32 states, decreased in two states and was essentially unchanged in 16 states, including the District of Columbia. The largest job gains occurred in California (+145,500), Texas (+118,100) and Florida (+51,600).

Below are a few key data points explained in further detail throughout the report:

- The October Manufacturing PMI® registered 59.3%, up 3.9 percentage points from the September reading of 55.4% and the highest since September 2018 (59.3%).

- The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in October on a seasonally adjusted basis after rising 0.2% in September, according to the U.S. Bureau of Labor Statistics. The all items index increased 1.2% (before seasonal adjustment) over the last 12 months, a slightly smaller increase compared to the 1.4% rise for the 12-month period ending September.

- Notable job gains occurred in leisure and hospitality, professional and business services, retail trade, as well as construction; employment in government declined.

- The Consumer Sentiment Index finished at 81.8 in October. However, the index is trending down (77.0) in November’s preliminary reading conducted by the University of Michigan Survey of Consumers.

- New vehicle sales are forecast to hit 1.36 million units, up 1.7% compared to October 2019. When compared to last month, sales are expected to increase approximately 25,000 units or nearly 1.9%.

- Average transaction prices are expected reach another all-time high, rising 7.3% to $36,755.

- The combination of elevated retail sales and average transaction prices means that consumers are expected to spend $43.7 billion on new vehicles, a record for the month of October.

- The mid-month Manheim Used Vehicle Value Index is 162.5, a year-over-year increase of 16.9%.

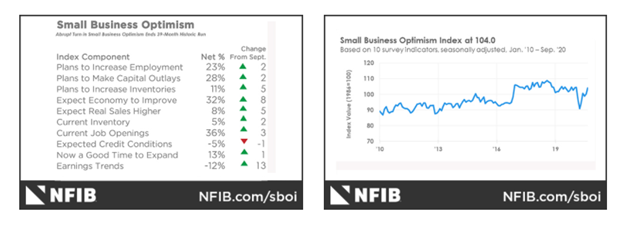

- The NFIB Optimism Index remained at 104 in October, unchanged from September and a historically high reading.

Four of the 10 components improved, five declined and one was unchanged. Although all of the data was collected prior to Election Day, a six-point increase in the NFIB Uncertainty Index to 98 was likely driven by the election and uncertain conditions in future months due to the COVID-19 pandemic and possible government-mandated shutdowns, according to NFIB. The uncertainty reading was the highest reading since November 2016.

“Leading up to the presidential election, small businesses continued to focus on stabilizing their businesses but were uncertain about the future economic conditions due to COVID-19 government regulations on all levels,” said Bill Dunkelberg, NFIB chief economist. “We see solid momentum going into the 4th quarter, and another good quarter could get the GDP back to its 2019 closing levels.”

Readers are encouraged to study the most current Small Business Optimism Index.

Important takeaways, courtesy of NFIB

- Earnings trends over the past three months improved nine points to a net negative 3% reporting higher earnings.

- Earnings trends have improved to pre-crisis levels, up 32 points since June.

- Inventory investment plans for the next three to six months increased one point to a net 12%, a record high.

- Real sales expectations in the next three months increased three points to a net 11% expecting gains.

- Owners expecting better business conditions over the next six months declined five points to a net 27%.

The monthly Key Performance Indicator Report is your comprehensive source for industry insights, exclusive interviews, new and used vehicle data, manufacturing summaries, economic analysis, consumer reporting, relevant global affairs and more. We value your readership.