KPI – January 2024: The Brief

A broad consensus of improved sentiment showed across age, income, education & geography lines…

KPI – January 2024: Recent Vehicle Recalls

KPI – January 2024: State of Manufacturing

KPI – January 2024: State of Business

KPI – January 2024: State of the Economy

KPI – January 2024: Consumer Trends

The Conference Board Consumer Confidence Index increased from a downwardly revised 101.0 in November to 110.7 (1985=100) in December. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – rose from 136.5 last month to 148.5 (1985=100) in December. Likewise, the Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – increased from a downwardly-revised reading of 77.4 in November to 85.6 (1985=100) in December.

Similarly, the University of Michigan Survey of Consumers – a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions – increased to 78.8, a 13% month-over-month increase.

“Like December, there was a broad consensus of improved sentiment across age, income, education and geography. Democrats and Republicans alike showed their most favorable readings since summer of 2021,” affirms Joanne Hsu, director of the University of Michigan Surveys of Consumers.

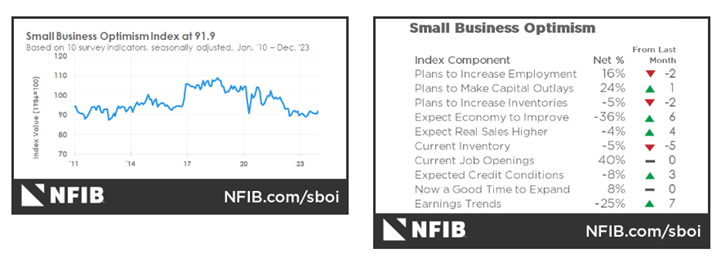

In addition, the NFIB Small Business Optimism Index increased 1.3 points in December (91.9) – a welcome boost but still the 24th consecutive month below a 50-year average of 98. Twenty-three percent of small business owners reported inflation as their single most important problem in operating the business – up one point from last month and replacing labor quality as the top concern. As a result of inflation, 25% reported raising average selling prices.

Moreover, 55% of owners reported hiring or trying to hire in December, with 89% of owners reporting “few or no qualified applicants” for the positions they were trying to fill. Approximately 33% have openings for skilled workers and 14% have openings for unskilled labor. The difficulty in filling open positions is particularly acute in the construction and transportation sectors.

“Small business owners remain very pessimistic about economic prospects this year,” says Bill Dunkelberg, chief NFIB economist. “Inflation and labor quality have consistently been a tough complication for small business owners, and they are not convinced that it will get better in 2024.”

Recently, Fiserv, Inc. (NYSE: FI) – a global provider of payments and financial services technology – launched the Fiserv Small Business Index. Company representatives describe the index as “a first-of-its-kind indicator” for assessing the performance of small businesses across the U.S., from national and state to industry levels.

“Small businesses are the backbone of our economy, generating 44% of U.S. gross domestic product (GDP) and accounting for almost half of all jobs in the country,” says Frank Bisignano, chairman, president and chief executive officer at Fiserv. “With the Fiserv Small Business Index, we are delivering swift, comprehensive and actionable intelligence based on consumer spending activity – providing a reliable new signal of the performance of U.S. small businesses.”

According to Fiserv, the index is differentiated by its direct aggregation of consumer spending activity within the U.S. small business ecosystem. Rather than relying on survey or sentiment figures, Bisignano says the Fiserv Small Business Index is derived from clear point-of-sale data, including in-store and online card, cash and check transactions from approximately 2 million U.S. small businesses.

Each month, the Fiserv Small Business Index will publish the data and analysis to help business owners, lenders, policymakers, economists, analysts and investors understand the trajectory of certain sectors within the small business network, benchmark sales performance, make well-informed decisions and adapt to an ever-changing market.

According to the December 2023 Fiserv Small Business Index, spending at small businesses ended the year with “a modest upswing.” Spending increased one point in December 2023 with an index reading of 138 (a 0.6% month-over-month increase and a 2.6% year-over-year increase).

“Small business sales gains in December reflected consumers’ priorities as the end of the year approached – food and drink, retail and healthcare,” says Prasanna Dhore, chief data officer at Fiserv. “The biggest increases in small business spending came from restaurants, clothing and related accessories, as well as ambulatory healthcare services.”

Nationally, the Fiserv Small Business Index for Retail registered 142 – unchanged from November. Sales across the retail sector declined marginally month-over-month – down -0.3% but up +1.6% year-over-year. Fiserv says the Clothing/Accessories/ Shoes/Jewelry sub-sector performed especially well, with sales up +6.1% month-over-month and +5% year-over-year.

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report.

Top Takeaways:

- Economic activity in the manufacturing sector contracted in December for the 14th consecutive month following a 28-month period of growth, according to the nation’s supply executives in the latest Manufacturing ISM Report On Business. The Manufacturing PMI registered 47.4% in December, up 0.7 percentage point from 46.7% in November.

- In December, the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.3% on a seasonally adjusted basis after rising 0.1% in November, according to the U.S. Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 3.4% before seasonal adjustment.

- Total new-vehicle sales for December 2023, including retail and non-retail transactions, are projected to reach 1,396,700 units – a 13.2% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

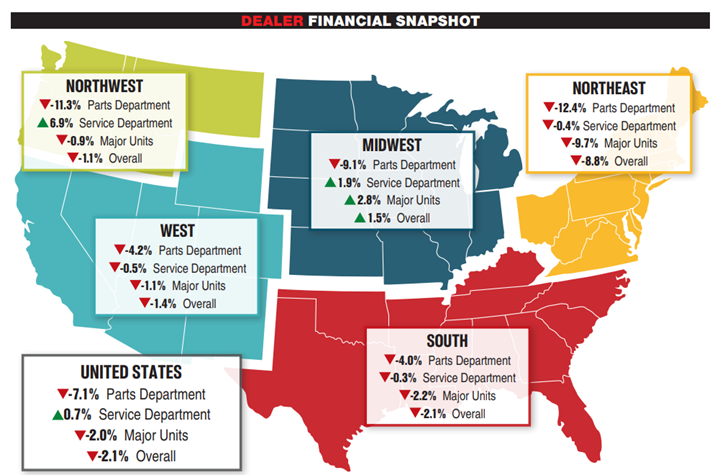

- Powersports Business says dealers across the country reported an overall revenue decline of 2.1% in December, according to composite data from more than 1,700 dealerships in the U.S. that utilize CDK Lightspeed DMS. On average, dealerships were down 2% in major units and 7.1% in the parts department.