KPI — May 2023: State of Business

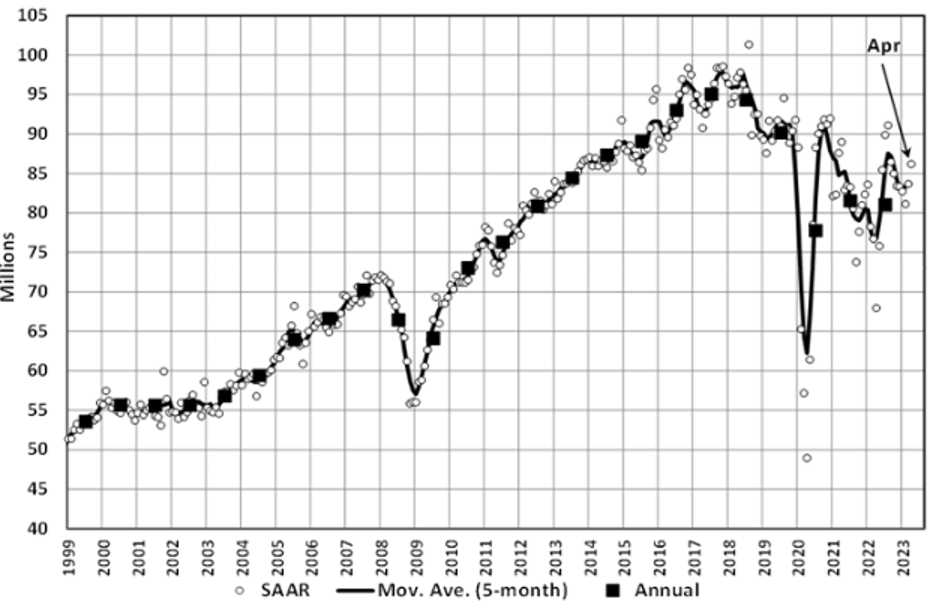

LMC Automotive reports Global Light Vehicle (LV) sales volume rose to 86 million units per year in April. More countries point to “easing supply shortages,” as evidenced by 25% year-over-year growth. The U.S., Western and Eastern Europe experienced positive year-over-year growth.

“Growth in China is an outlier at a projected increase of 90% from being locked down in April 2022. Solid growth continues in Europe, up 21.5%, as markets start to rebound from supply disruption and the effect of the war in Ukraine,” says Jeff Schuster, president of global forecasts at LMC Automotive.

“Supply disruption is projected to improve further but will remain an issue throughout 2023. The overall effect on underlying demand is expected to be 4 million units of disruption, half what it was in 2022,” Schuster adds.

State of Manufacturing

Economic activity in the manufacturing sector contracted in April for the sixth consecutive month following a 28-month period of growth, according to the nation’s supply executives in the latest Manufacturing ISM® Report On Business®. The April Manufacturing PMI® registered 47.1%, 0.8 percentage point higher than the 46.3% recorded in March.

“The U.S. manufacturing sector contracted again; however, the Manufacturing PMI® improved compared to the previous month, indicating slower contraction. The April composite index reading reflects companies continuing to manage outputs to better match demand for the first half of 2023 and prepare for growth in the late summer/early fall period,” says Timothy R. Fiore, CPSM, C.P.M., chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Important takeaways, Courtesy of the Manufacturing ISM® Report On Business®:

- Demand eased, with the (1) New Orders Index contracting, though at a slower rate; (2) New Export Orders Index is slightly below 50% but improving; (3) Customers’ Inventories Index is entering the low end of ‘too high’ territory, a negative for future production; and (4) Backlog of Orders Index continues in strong contraction.

- Output/Consumption (measured by the Production and Employment indexes) was positive, with a combined 4.4-percentage point upward impact on the Manufacturing PMI® calculation.

- The Employment Index indicated slight expansion after two months of contraction, and the Production Index logged a fifth month in contraction territory – though at a slightly slower rate.

- Inputs – defined as supplier deliveries, inventories, prices and imports – continue to accommodate future demand growth.

- The Supplier Deliveries Index indicated faster deliveries, and the Inventories Index dropped further into contraction as panelists’ companies manage inventories exposure.

- The Prices Index moved back into ‘increasing’ territory, though at a moderate level, after one month of marginally decreasing prices.

U.S. New Vehicle Sales

Total new vehicle sales for April 2023, including retail and non-retail transactions, are projected to reach 1,316,500 units – a 9.8% year-over-year increase, according to a joint forecast from J.D. Power and LMC Automotive.

“The industry is poised for another favorable month in April, with projected retail sales expected to increase 5.9%, accompanied by a 2% increase in average transaction prices,” says Thomas King, president of the data and analytics division at J.D. Power. “With the significant improvement in overall new vehicle availability from a year ago, dealer margins are declining and manufacturer incentive spending is increasing. Nevertheless, the demand for vehicles in the retail market remains strong due to pent-up demand from pandemic-related production shortages.”

However, he says the retail sales pace continues to be supply constrained. As such, pricing and profitability remain well above historical levels.

“This market condition is being sustained by manufacturers allocating more production volume to fleet sales,” King explains. “Rather than allocating all incremental production to retailers, manufacturers are opting to sell more vehicles to fleet customers, with fleet sales projected to increase 33% vs. April 2022.”

Important Takeaways, Courtesy of J.D. Power:

- Retail buyers are on pace to spend $47.5 billion on new vehicles, up $1.3 billion year-over-year.

- Truck/SUVs account for 78% of new vehicle retail sales in April.

- The average new vehicle retail transaction price is expected to reach $46,044, a 2% year-over-year increase. The previous high for any month was $47,362, set in December 2022.

- Average interest rates for new-vehicle loans are expected to increase to 6.85%, 227 basis points higher than a year ago.

- Total retailer profit per unit, which includes grosses and finance and insurance income, is expected to reach $3,755. While this is 24.5% lower than a year ago, it is still more than double the amount of April 2019.

- Fleet sales are expected to total 229,100 units in April, up 33.3% year-over-year on a selling day adjusted basis. Fleet volume is expected to account for 17% of total light vehicle sales, up from 14% year-over-year.

“As we look to May, the asymmetrical market positions of each manufacturer could become more apparent. Brands with higher inventory levels may participate in the tradition of Memorial Day promotions and discounts to generate sales, while other brands that are still struggling with production will have to decide whether or not to compete on price. The disparity in inventory may result in unbalanced year-over-year sales results among manufacturers,” King says.

“Despite these challenges, including elevated interest rates, consumer demand has demonstrated remarkable resilience. Therefore, we can anticipate that manufacturers and retailers will continue to benefit from historically high profitability on the vehicles they sell.”

U.S. Used Market

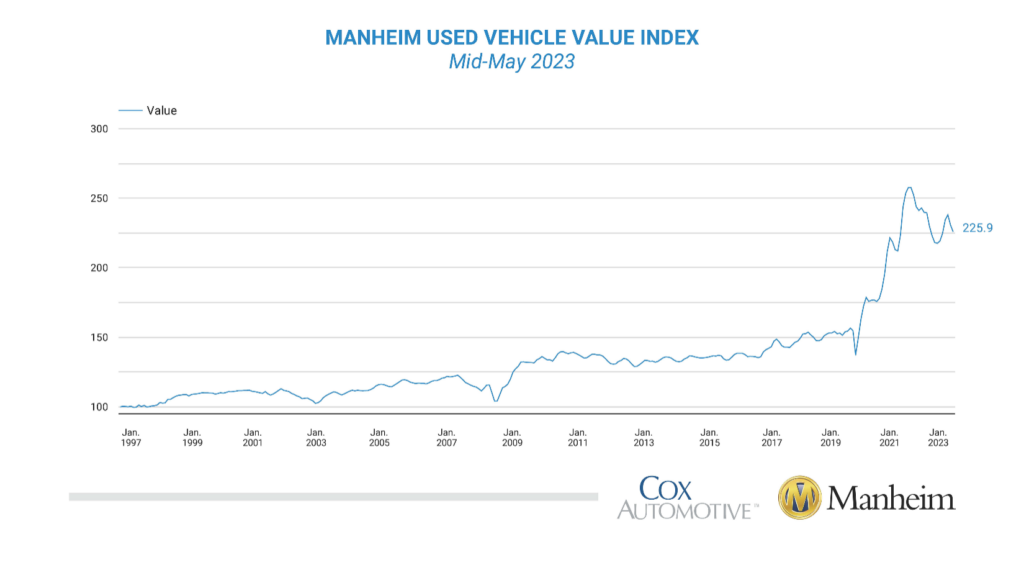

Wholesale used-vehicle prices (on a mix-, mileage- and seasonally-adjusted basis) decreased 2.1% from April in the first 15 days of May. The mid-month Manheim Used Vehicle Value Index dropped to 225.9 – down 7% year-over-year.

According to Manheim, all eight major market segments posted seasonally-adjusted prices that were lower year-over-year in the first half of May. In fact, only pickups and compact cars (3.9% and 6.6%, respectively) lost less compared to the overall industry in seasonally adjusted year-over-year changes. The remaining segments declined between 7.4% and 14.3%, with sports cars dipping the most. Seven of the eight major segments saw price decreases compared to April, with losses ranging from 1.7% to 7%, while vans were flat.

Used vehicle price declines are resulting in less trade-in equity for new-vehicle buyers. Currently, JD Power says the average trade-in equity is approximately $9,162 – down $363 from a year ago and $908 since the peak in June 2022. For context: trade equity is more than double the pre-pandemic level, thus helping owners with a vehicle to trade in offset some of the pricing and interest rate hikes.

KPI — May 2023: Recent Vehicle Recalls

Key Performance Indicators Report — May 2023