- KPI – March 2025: Consumer Trends

- KPI – March 2025: State of Manufacturing

- KPI – March 2025: State of Business – Automotive Industry

- KPI – March 2025: State of the Economy

- KPI – March 2025: Recent Vehicle Recalls

The Conference Board Consumer Confidence Index dropped to 98.3 in February. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – fell 3.4 points to 136.5. Meanwhile, the Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – declined 9.3 points to 72.9.

The University of Michigan Survey of Consumers also posted a month-over-month decline, sliding from a dismal 64.7% in February to an even lower preliminary reading of 57.9% in March. Joanne Hsu, survey director, says the decline is consistent across all groups by age, education, income, wealth, political affiliations and geographic regions.

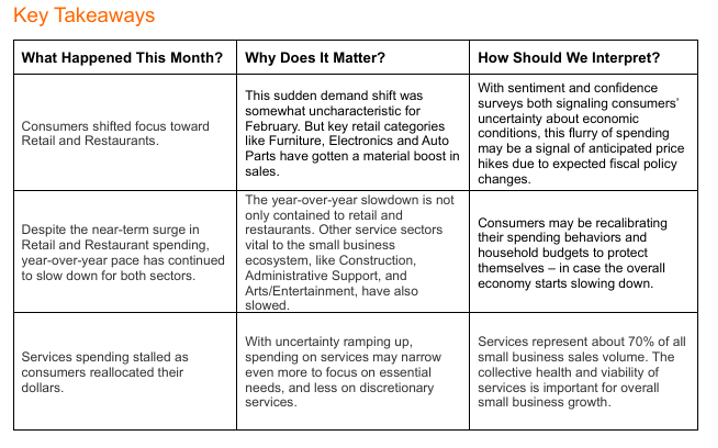

While consumers across the country are feeling the heat with rising rent, utilities and insurance, alongside elevated grocery costs and fluctuating mortgage rates, some key data points shine brightly.

The seasonally adjusted Fiserv Small Business Index registered 147 in February 2025, in line with previous month data. The transaction index gained 1 point, reaching 114. Sales growth was flat overall (+0.1%) compared to January. At +2.1%, year-over-year sales growth slowed considerably compared to a seasonally adjusted pace of +4.9% a month prior. Moreover, while transactions accelerated by +1.6% month-over-month, they slowed to +4% year-over-year versus +6.4% last month.

Growth in small businesses proved to be broad, with the strongest monthly spending gains in Restaurants, Sporting Goods, Auto Parts, Furniture and Clothing. On the contrary, service-oriented spending declined in the areas of Professional Services, Administrative and Support Services, Performing Arts and Accommodation (Hotels). Food and Beverage Retailers also declined compared to January.

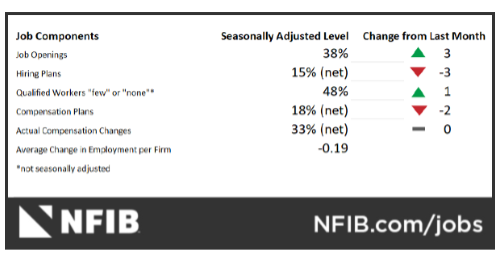

At 100.7, the NFIB Small Business Optimism Index supports the trend in elevated small business confidence. While the index dipped 2.1 points in February, it is the fourth consecutive month above the 51-year average of 98, following 34 consecutive months below the five-decade average.

To put the index in greater perspective, small business confidence was 91.2 in August 2024, 91.5 in September 2024, 93.7 in October 2024, 101.7 in November 2024, 105.1 in December 2024 and 102.8 in January 2025. Even with the slight decline, this month’s index is well above the 97.6 average during the past six months. That said, economists warn recent progress is threatened by ongoing uncertainty.

“Uncertainty is high and rising on Main Street, and for many reasons,” says Bill Dunkelberg, NFIB chief economist. “Those small business owners expecting better business conditions in the next six months dropped and the percent viewing the current period as a good time to expand fell, but remains well above where it was in the fall. Inflation remains a major problem, ranked second behind the top problem – labor quality.”

Important takeaways, courtesy of NFIB:

- The net percent of owners expecting the economy to improve fell 10 points to a net 37% (seasonally adjusted).

- Twelve percent (seasonally adjusted) of owners reported that it is a good time to expand their business, down 5 points from January and the largest monthly decrease since April 2020.

- Sixteen percent of owners reported that inflation was their single most important problem in operating their business, down 2 points from January and now just below labor quality as the top issue. The last time it registered this low was in October 2021.

- The net percent of owners raising average selling prices rose 10 points to a net 32% (seasonally adjusted). This is the largest monthly increase since April 2021, and the third highest in the survey’s history. The percent of owners lowering their prices is 10 points lower than it was one year ago.

- Seasonally adjusted, a net 29% plan price hikes in the next three months – up three points from January and the highest reading in 11 months.

- Labor costs reported as the single most important problem for business owners, rising 3 points to 12%, only one point below the survey’s highest reading of 13% reached in December 2021. The last time labor costs ranked this high was in February 2023.

- The frequency of reports of positive profit trends was a net negative 24% (seasonally adjusted), up 1 point from January.

- A net 2% of owners reported that their last loan was harder to get than in previous attempts (down 1 point). The last time the reading was this low was in February 2022.

- Twenty-four percent of all owners reported borrowing on a regular basis, down 3 points from January and the lowest since May 2022.

Image Source: NFIB Small Business Optimism Index

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report.

Key data points:

- Economic activity in the manufacturing sector expanded for the second month in a row in February after 26 consecutive months of contraction, say the nation’s supply executives in the latest Manufacturing ISM Report On Business. The Manufacturing PMI registered 50.3% in February, 0.6 percentage point lower compared to the 50.9% recorded in January.

- In February, the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.2% on a seasonally adjusted basis following a 0.5% increase in January. Over the last 12 months, the all-items index increased 2.8% before seasonal adjustment.

- Total new-vehicle sales for January 2025, including retail and non-retail transactions, are projected to reach 1,105,900 – a 4.4% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

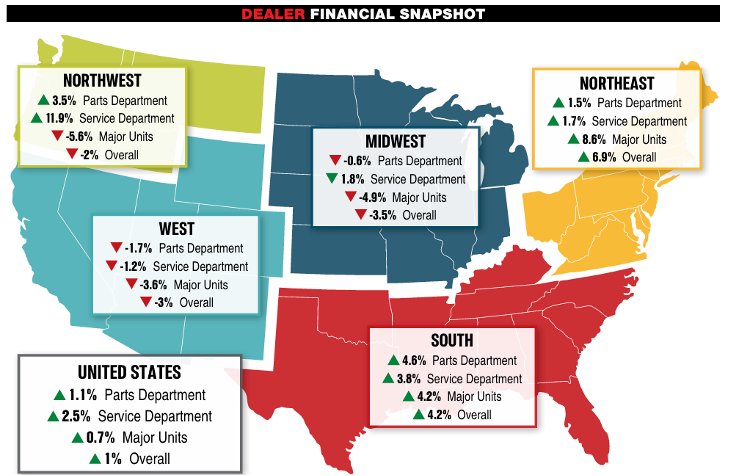

- Powersports Business says dealers across the country reported an overall combined revenue incline of 1% year-over-year in January, according to composite data from more than 1,700 dealerships in the U.S. that utilize CDK Lightspeed DMS. On average, dealerships were up 0.7% in major units, 2.5% in service and 1.1% in parts.

Image Source: Powersports Business