- KPI – March 2025: The Brief

- KPI – March 2025: Recent Vehicle Recalls

- KPI – March 2025: State of Business – Automotive Industry

- KPI – March 2025: State of the Economy

- KPI – March 2025: Consumer Trends

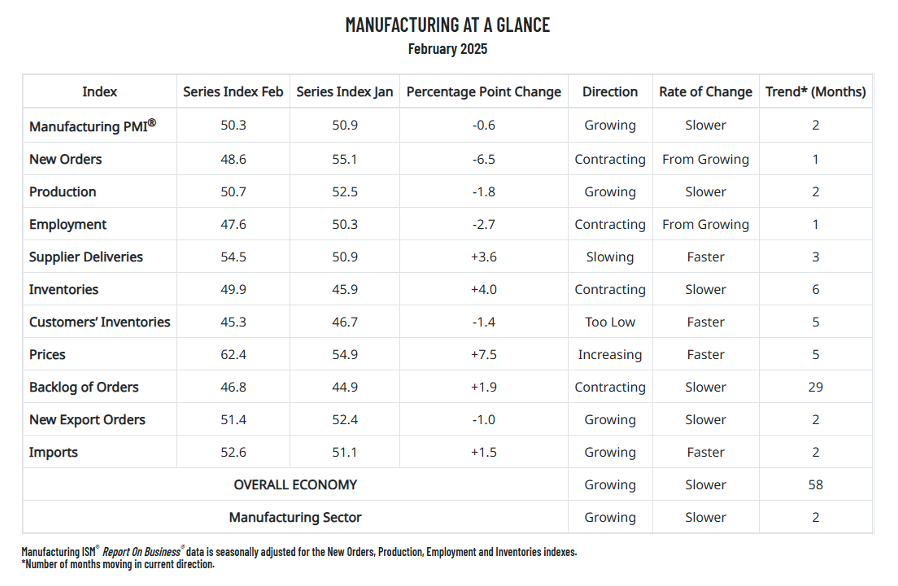

Economic activity in the manufacturing sector expanded for the second month in a row in February after 26 consecutive months of contraction, say the nation’s supply executives in the latest Manufacturing ISM Report On Business. The Manufacturing PMI registered 50.3% in February, 0.6 percentage points lower compared to the 50.9% recorded in January.

“Demand eased, production stabilized and de-staffing continued as panelists’ companies experience the first operational shock of the new administration’s tariff policy. Prices growth accelerated due to tariffs, causing new order placement backlogs, supplier delivery stoppages and manufacturing inventory impacts. Although tariffs do not go into force until mid-March, spot commodity prices have already risen about 20%,” says Timothy R. Fiore, CPSM, C.P.M., chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee.

Important Takeaways, Courtesy of the Manufacturing ISM Report On Business

- Demand weakened, output stabilized and inputs contributed to PMI growth for the first time in several months. Indications that demand weakened include: the (1) New Orders Index dropped into contraction territory; (2) New Export Orders Index continued expanding, though at a slower rate; (3) Backlog of Orders Index continued in contraction but moved upward; and (4) Customers’ Inventories Index moved further into “too low” territory.

- Output (measured by the Production and Employment indexes) was stable. Factory output marginally expanded compared to January, indicating that panelists’ companies are being cautious about ramping up output in the face of economic headwinds. The Employment Index moved back into contraction, as panelists’ companies continued to release workers. More companies cited “attriting down” as the best process, with de-staffing not as urgent as it was in the second half of 2024.

- Inputs – defined as supplier deliveries, inventories, prices and imports – revealed the first signs of supplier difficulties due to some pull-forward deliveries and discussions about who will pay for tariffs. Inventories recovered somewhat as a result.

What Respondents Are Saying, According to the Manufacturing ISM Report On Business

- “The tariff environment regarding products from Mexico and Canada has created uncertainty and volatility among our customers and increased our exposure to retaliatory measures from these countries.” [Chemical Products]

- “Customers are pausing on new orders as a result of uncertainty regarding tariffs. There is no clear direction from the administration on how they will be implemented, so it’s harder to project how they will affect business.” (Transportation Equipment)

- “Tariff impact has been minimal to overall manufacturing and raw material supply. Limits on U.S. government spending in key organizations like the Food and Drug Administration, Environmental Protection Agency and National Institutes of Health are delaying some orders.” (Computer & Electronic Products)

- “Inflation and pricing pressure continue to drive uncertainty in our 2025 outlook. We are seeing volume impacts due to pricing, with customers buying less and looking for substitution options.” (Food, Beverage & Tobacco Products)

- “The incoming tariffs are causing our products to increase in price. Sweeping price increases are incoming from suppliers. Most are noting increases in labor costs. Vendors are indicating open capacity. Inflationary pressures are a concern. Our company is working diligently to see how the new tariffs will affect our business.” (Machinery)

- “Business is still slow, but some indications of improved demand are six to nine months out. Steel and scrap costs are increasing, and it’s too early to tell how high they will go.” (Fabricated Metal Products)

- “New orders continue to be strong after picking up in December. The uncertainty about tariffs keeps us cautious on spending, despite the strong sales right now.” (Electrical Equipment, Appliances & Components)

- “Management now has us running scenarios to project tariff impacts to our business. They want numbers in 24 hours on variables that equate to a wild guess. Interesting times we live in.” (Nonmetallic Mineral Products)

- “Internal analysis ongoing about impact of tariffs, but nothing concrete yet. General business conditions remain tepid; outlook on the durables side growing more pessimistic with growing domestic inventories of automobiles.” (Plastics & Rubber Products)

- “Customer volumes seem to be better than 2024. However, customers are still very hesitant to commit to long-term volumes due to the market uncertainty caused by proposed tariffs on steel/aluminum imports.” (Primary Metals)