- KPI – June 2025: State of Business – Automotive Industry

- KPI – June 2025: State of Manufacturing

- KPI – June 2025: State of the Economy

- KPI – June 2025: Consumer Trends

- KPI – June 2025: Recent Vehicle Recalls

While confidence and sentiment survey data reflect uncertainty and angst, with consumers and business leaders alike bracing for maximum tariff impact or cooling in the job market, key indicators point to a robust and resilient U.S. economy.

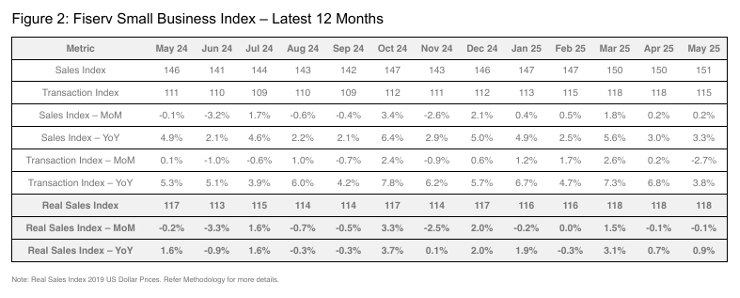

The seasonally adjusted Fiserv Small Business Index registered 151 in May, a nominal increase of 0.2% month-over-month and up 3.3% year-over-year. The Fiserv Small Business Transaction Index stood at 115.0, with transactions dipping 2.7% month-over-month but up 3.8% year-over-year.

Key Takeaways, Courtesy of The Fiserv Small Business Sales Index:

- Overall, consumer spending across small businesses remains resilient year-over-year. Topline sales grew 3.3% compared to May 2024, with inflation-adjusted growth still positive at 0.9%. Consumers were more conservative in their spending compared to April. Month-over-month sales growth was relatively unchanged at +0.2% in May, and -0.1% when adjusted for inflation.

- Essential sales grew 4.7% year-over-year, outpacing discretionary spending growth of 1.8%. Near-term, essential sales dipped -0.1% month-over-month, while discretionary sales rose 0.5%. Higher average tickets (+4.2% for discretionary, +0.4% for essential) drove these increases, as transactions fell month-over-month (-3.7% for discretionary, -0.5% for essential).

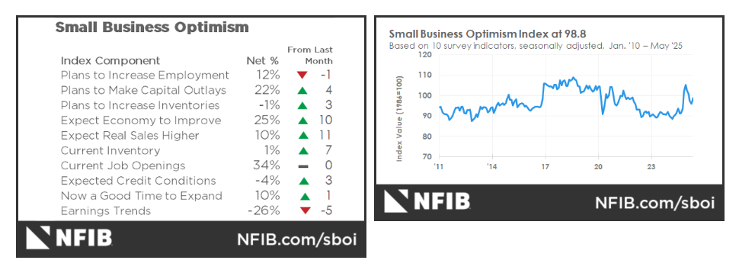

The NFIB Small Business Optimism Index increased by three points in May to 98.8, slightly above the 51-year average of 98. Expected business conditions and sales expectations contributed the most to the rise in the index. Likewise, the Uncertainty Index rose two points from April to 94. Approximately 18% of small business owners reported taxes as their single most important problem, up two points from April and ranking as the top problem. According to NFIB, the last time taxes were ranked as the top single most important problem was in December 2020.

“Although optimism recovered slightly in May, uncertainty is still high among small business owners. While the economy will continue to stumble along until the major sources of uncertainty are resolved, owners reported more positive expectations on business conditions and sales growth,” says Bill Dunkelberg, NFIB chief economist.

Important Takeaways, Courtesy of NFIB:

- A net 1% (seasonally adjusted) of owners viewed current inventory stocks as “too low” in May, up 7 points from April and the highest reading since August 2022. This was the largest monthly increase in the survey’s history.

- The net percent of owners expecting better business conditions rose 10 points to a net 25% (seasonally adjusted).

- The net percent of owners expecting higher real sales volumes rose 11 points to a net 10% (seasonally adjusted). This component contributed the most to the Optimism Index’s improvement.

- Twenty-two percent (seasonally adjusted) plan capital outlays in the next six months, up four points and the highest reading of this year.

- The percentage of small business owners reporting labor quality as the single most important problem for business fell three points to 16%.

- Fourteen percent of owners reported inflation as their single most important problem in operating their business, unchanged from April.

- When asked to rate the overall health of their business, 14% reported excellent (up one point), and 55% reported good (down one point). Twenty-eight percent reported the health of their business was fair (up one point) and 4% reported poor (unchanged).

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report.

Key Data Points:

- Economic activity in the manufacturing sector contracted in May for the third consecutive month, following a two-month expansion preceded by 26 straight months of contraction, according to the nation’s supply executives in the latest Manufacturing ISM Report On Business.

- In May, the Consumer Price Index for All Urban Consumers (CPI-U) increased 0.1% on a seasonally-adjusted basis following a 0.2% rise in April, according to the U.S. Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 2.4% before seasonal adjustment.

- In May, the Global Light Vehicle (LV) selling rate is estimated to hit 90 million units per year, a slowdown from the improvement observed last month. In addition, the market grew 5% year-over-year, as sales reached 7.6 million units globally. Total new vehicle sales for June 2025, including retail and non-retail transactions, are projected to reach 1,247,900—a 2.5% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

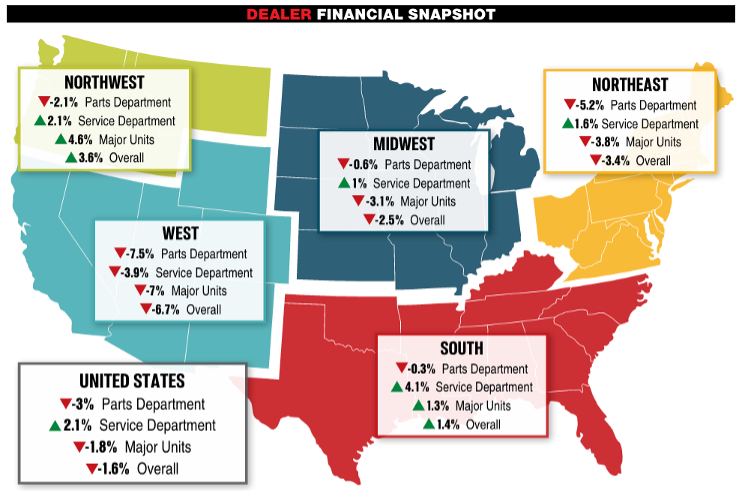

- Powersports Business says dealers across the country reported an overall combined revenue decline of 1.6% year-over-year in May, according to composite data from more than 1,700 dealerships in the U.S. that utilize CDK Lightspeed DMS. On average, dealerships were down 1.8% in major units and 3% in parts, but up 2.1% in service.