- KPI – January 2026: The Brief

- KPI – January 2026: State of Business – Automotive Industry

- KPI – January 2026: State of the Economy

- KPI – January 2026: Consumer Trends

- KPI – January 2026: Recent Vehicle Recalls

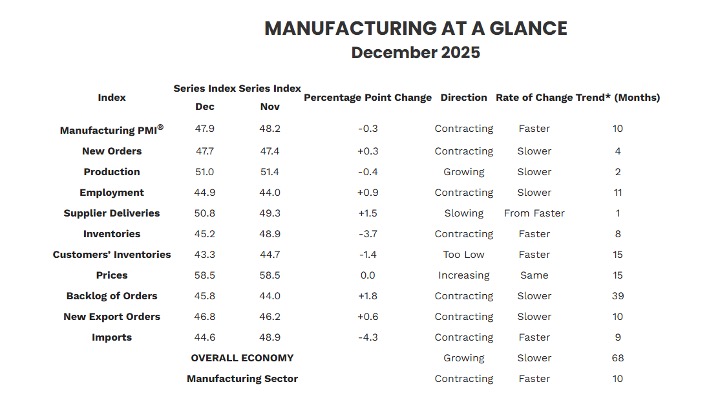

Economic activity in the manufacturing sector contracted in December for the 10th consecutive month, following a two-month expansion preceded by 26 straight months of contraction, according to the nation’s supply executives in the latest ISM Manufacturing PMI Report. The Manufacturing PMI registered 47.9% in December, the lowest reading of 2025.

“In December, U.S. manufacturing activity contracted at a faster rate, with pullbacks in the Production and Inventories indexes leading to the 0.3-percentage point decrease of the Manufacturing PMI. Those two subindexes increased in November, so their contraction this month continues the short-term ‘bubble’ of improvement indicative in the last several months of PMI data—and a hallmark of recent economic uncertainty in manufacturing,” says Susan Spence, MBA, chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee.

Data shows 85% of the sector’s gross domestic product (GDP) contracted in December, compared to 58% in November. Moreover, the percentage of manufacturing GDP in strong contraction (defined as a composite PMI of 45% or lower) increased from 39% in November to 43% in December.

“The share of sector GDP with a PMI at or below 45% is a good metric to gauge overall manufacturing weakness. Of the six largest manufacturing industries, only Computer & Electronic Products expanded in December,” Spence says.

Important Takeaways, Courtesy of the Manufacturing ISM Report On Business:

- The demand indicators remain in contraction, but improvement in three indexes (New Orders, Backlog of Orders, and New Export Orders) and the Customers’ Inventories Index remaining in “too low” territory (and at an accelerated rate) are positive signs for December. Several consecutive months of gains in these indicators are necessary for a longer-term recovery. A “too low” status for the Customers’ Inventories Index is usually considered positive for future production.

- Regarding output, the Production Index is still in expansion but slipped 0.4%. This is likely due to last month’s drop in the New Orders and Backlog of Orders indexes. The Employment Index contracted at a slower pace, with 63% of panelists indicating that managing headcounts is still the norm at their companies, as opposed to hiring.

- Inputs (defined as supplier deliveries, inventories, prices and imports) were mixed, with the Supplier Deliveries Index indicating slower deliveries, the Inventories and Imports indexes contracting strongly, and the Prices Index with the same reading as in November.

What Respondents Are Saying:

- “Winding up the year with mixed results. It has not been a great year. We have had some success holding the line on costs; however, real consumer spending is down and tariffs are ultimately to blame. I hope for some return to free trade, which is what consumers have voted for with their spending.” [Chemical Products]

- “Through conditions continue: depressed business activity, some seasonal but largely impacted by customer issues due to interest rates, tariffs, low oil commodity pricing and limited housing starts.” [Machinery]

- “Things are quieter regarding tariffs, but prices for all products remain higher. Our costs have increased, so we have increased prices for our customers to compensate. Margins have deteriorated, as full pass-through (of cost increases) is not possible.” [Computer & Electronic Products]

- “Things are not improving in the transportation equipment market. Many customers are ordering for 2026, but those orders are 20%-30% below their historical buying patterns. Some large fleets are still completely on hold for 2026, with zero capital expenditures money available to fleet budgets. Truck rental utilization, which is a good benchmark for the health of the economy, is still below historically stable levels. The general mood of the industry is that the first half of 2026 will be another bust, and we’re now hoping things pick up in the second half, even as the North American truck fleet continues to age.” [Transportation Equipment]

- “In the current environment, our company is struggling with customer orders and financially overall. Our senior leaders are struggling to focus our business and get the company on track with quality products. In November, layoffs impacted about 9% of our workforce, affecting all locations in the U.S. and Europe.” [Machinery]

- “Orders continue to drop for most of our businesses. Many plants are not running near full capacity. Make to order being utilized where possible.” [Chemical Products]

- “Order levels have continued to decline: We had a bad October, an awful November and a dismal December. January and February don’t look too good, as bookings are down 25% compared to the first two months of 2025.” [Fabricated Metal Products]

- “Morale is very low across manufacturing in general. The cost of living is very high, and component costs are increasing, with folks citing tariffs and other price increases. It’s cold in our area of the country, absenteeism is worse around the holidays, and sales were lower than we expected for November. So, things look a bit bleak overall.” [Electrical Equipment, Appliances & Components]

- “Global logistics remain sensitive to geopolitical shifts. Tariffs are influencing equipment pricing and procurement strategies. Large-scale data center programs are absorbing and reducing availability of resources for other sectors.” [Food, Beverage & Tobacco Products]

- “2025 revenue was down 17% due to tariffs. The lost revenue has inhibited our ability to offer bonuses to employees or create and hire for new positions.” [Miscellaneous Manufacturing]