KPI — January 2022: State of Business — Automotive Industry

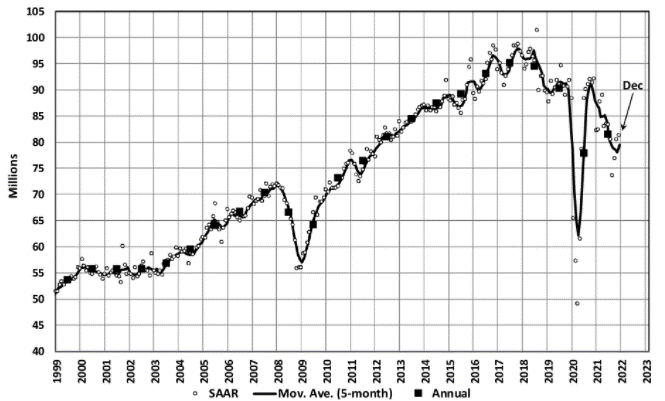

Global Light Vehicle (LV) sales are estimated to tally 81 mn units/year in 2021. Despite a 5% year-over-year increase, the global market remains down 10% compared to 2019. Sitting at an 8% decline, China continues to outpace the world in recovery, said Jeff Schuster, president of Americas operations and global vehicle forecasts at LMC Automotive. Meanwhile, Europe is down 17%, and the U.S., Japan and South Korea are lagging at 16%.

“A mild improvement in the chip shortage may be overshadowed by risk from the surge in Omicron variant COVID-19 cases. While vehicle shortage and the inventory crunch appear to have peaked, they continue to have a negative effect on demand. The uncertainty of potential restrictions and lockdowns in Europe and Asia could be problematic for global sales levels as we enter 2022,” said Schuster.

Even with the added risk, Schuster said the global outlook improved to 86 million units in 2022. “We remain cautiously optimistic about the pace of recovery during the next 18 months,” he said.

The December Manufacturing PMI® registered 58.7%, a decrease of 2.4 percentage points from the November reading of 61.1%, according to supply executives in the latest Manufacturing ISM® Report On Business®.

“The U.S. manufacturing sector remains in a demand-driven, supply chain-constrained environment, with indications of improvements in labor resources and supplier delivery performance. Shortages of critical lowest-tier materials, high commodity prices and difficulties in transporting products continue to plague reliable consumption. Coronavirus pandemic-related global issues – worker absenteeism, short-term shutdowns due to parts shortages, employee turnover and overseas supply chain problems – continue to impact manufacturing,” said Timothy R. Fiore, CPSM, C.P.M., chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Important takeaways, courtesy of the Manufacturing ISM® Report On Business®:

- Demand expanded, with the (1) New Orders Index growing, supported by continued expansion of new export orders, (2) Customers’ Inventories Index remaining at a very low level and (3) Backlog of Orders Index staying at a very high level.

- Consumption (measured by the Production and Employment indexes) grew during the period, with a combined negative 1.4-percentage point change to the Manufacturing PMI® calculation.

- The Employment Index expanded for a fourth straight month, with some indications that ability to hire is improving, though somewhat offset by the continued challenges of turnover and backfilling.

- Inputs – expressed as supplier deliveries, inventories and imports – continued to constrain production expansion, but there are clear signs of improved delivery performance.

- The Supplier Deliveries Index again slowed while the Inventories Index expanded, both at a slower rate.

- The Prices Index increased for the 19th consecutive month, at a slower rate (a decrease of 14.2 percentage points), indicating that supplier pricing power continues to rise, but to a lesser degree.

“The ongoing supply-chain disruption has had ripple effects throughout the global economy, including the specialty-equipment industry,” affirmed Kyle Cheng, SEMA. In fact, he said more than 80% of industry companies reported severe or moderate impacts in 2021 due to production delays, shipping issues and higher prices.

Industry professionals are optimistic that 2022 will be a brighter year. SEMA Market Research projects most pressing issues within the global supply chain should improve in the second half of the year. However, according to the report, prices may remain elevated for longer and likely into 2023.

U.S. New Vehicle Sales

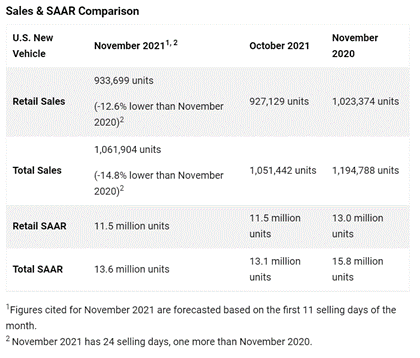

New vehicle retail sales are expected to decline year-over-year in December 2021, according to a joint forecast from J.D. Power and LMC Automotive.

New vehicle sales in December 2021, including retail and non-retail transactions, are projected to reach 1,245,600 units – a 20.5% decrease from December 2020.

“Despite inventory shortages constraining December sales volumes, there are several good news stories for the industry,” said Thomas King, president of the data and analytics division at J.D. Power. “Retail inventory is showing some improvement, tracking at just more than one million units for the first time since July and transaction prices and retailer profits are at record highs.”

Important Takeaways, Courtesy of J.D. Power:

- Buyers are on pace to spend $50.6 billion on new vehicles, down $2.3 billion year-over-year.

- Truck/SUVs are on pace to account for a record 80.2% of new vehicle retail sales in December.

- Average incentive spending per unit is expected to reach $1,598, down from $3,889 in December 2020.

- The average new vehicle retail transaction price is expected to reach $45,743. The previous high for any month was $44,515, set in November 2021.

- Total retailer profit per unit – inclusive of grosses and finance & insurance income – is on pace to reach a record $5,258, an increase of $3,277 from a year ago and a third consecutive month above $5,000.

- Fleet sales are expected to total 140,000 units in December, down 38.6% year-over-year on a selling day adjusted basis. Fleet volume is expected to account for 11% of total light-vehicle sales, down from 15% a year ago.

“Looking forward to 2022, retail sales will continue to be dictated by the number of vehicles shipped from plants and ports to dealerships. Indications are that shipments will rise incrementally as the year goes on, allowing sales to rise from 2021 levels,” said King. “However, pent-up consumer demand will keep inventory levels near historical lows. Therefore, 2022 is likely to be another year of record setting pricing and profitability.”

U.S. Used Market

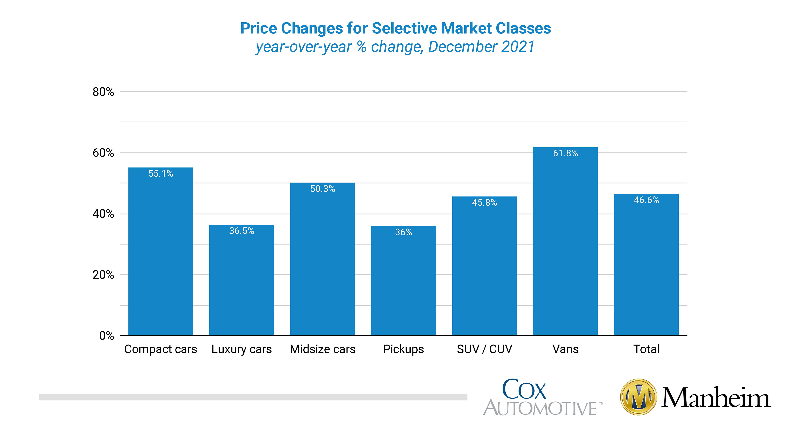

Wholesale used vehicle prices (on a mix-, mileage- and seasonally adjusted basis) increased 1.6% month-over-month in December – bringing the Manheim Used Vehicle Value Index to 236.2, a 46.6% increase from a year ago.

According to the most current data, Manheim Market Report (MMR) values saw weekly price decreases in December that accelerated in the final weeks of the month.

All major market segments saw year-over-year, seasonally adjusted price increases. Vans had the largest year-over-year performance, while the pickup, luxury car and SUV segments lagged the overall market, according to Manheim. On a month-over-month basis, no segment saw declines, as compact and luxury vehicles outpaced the market and remaining segments.

Cox Automotive estimates total used vehicle sales were down 4% year-over-year in December. The used SAAR is forecast to be 39.1 million, down from 40.6 million year-over-year and flat compared to November’s revised 39.1 million SAAR. The December used retail SAAR estimate is 20.4 million, down from 21.6 million last year and flat month-over-month, noted Cox Automotive.

KPI — January 2022: Recent Vehicle Recalls

Key Performance Indicators Report — January 2022