KPI — April: Manufacturing ISM

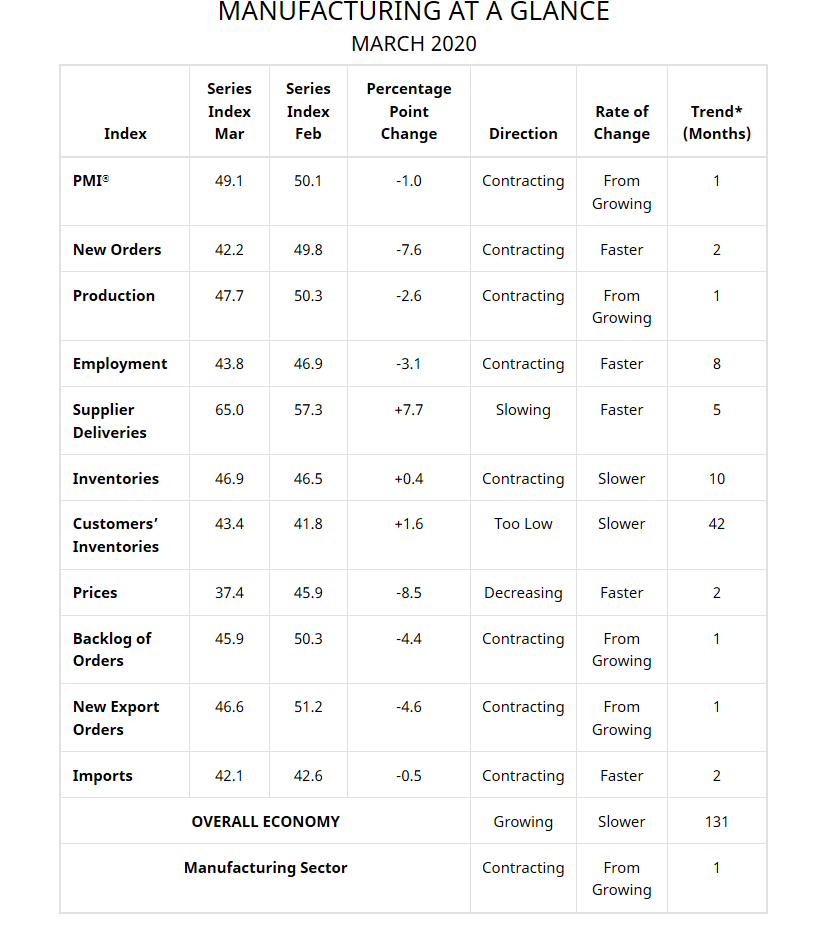

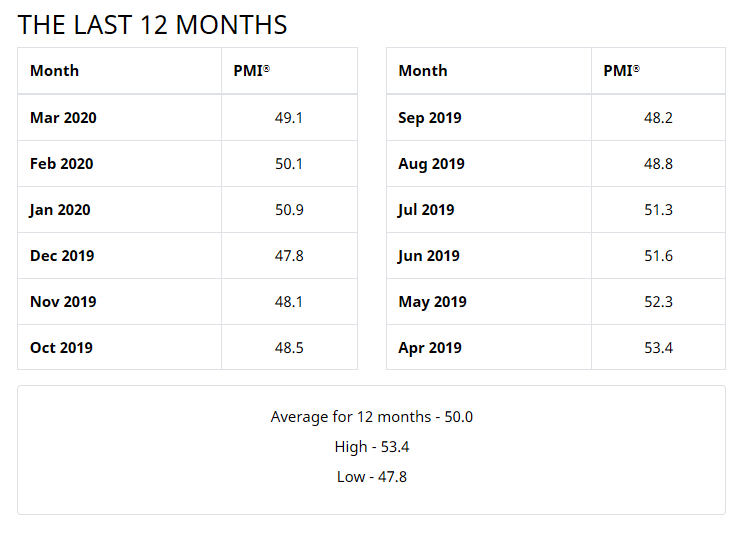

Economic activity in the manufacturing sector contracted in March, and the overall economy grew for the 131st consecutive month, say the nation’s supply executives in the latest Manufacturing ISM® Report On Business®. The March PMI® registered 49.1%, down one percentage point from the February reading of 50.1%.

The Report On Business® measures its data using the Purchasing Manager’s Index (PMI), which is an indicator of economic health in the manufacturing sector. A reading above 50% indicates that the manufacturing economy is generally expanding, while below 50% indicates that it is generally contracting.

“Comments from the panel were negative regarding the near-term outlook, with sentiment clearly impacted by the coronavirus (COVID-19) pandemic and energy market volatility. The PMI® returned to contraction territory, and with a negative trajectory,” said Timothy R. Fiore, CPSM, C.P.M., Chair of the Institute for Supply Management® (ISM®) Manufacturing Business Survey Committee.

Demand slumped, with (1) the New Orders Index contracting at a strong level, in part pushed by new export order contraction, (2) the Customers’ Inventories Index remaining at “too low” status, but increasing at a level considered a negative for future production and (3) the Backlog of Orders Index contracting again, at a moderate rate.

“The coronavirus pandemic and shocks in global energy markets have impacted all manufacturing sectors. Among the six big industry sectors, Food, Beverage & Tobacco Products remains strongest, followed by Chemical Products, which in addition to the pharmaceutical component, is a significant contributor to the Food, Beverage & Tobacco Products Industry and beneficiary of low energy and feedstock prices. Transportation Equipment and Petroleum & Coal Products are the weakest sectors. Sentiment regarding near-term growth this month is strongly negative, by a 2-to-1 ratio,” added Fiore.

Of the 18 manufacturing industries, 10 reported growth during March: Printing & Related Support Activities; Food, Beverage & Tobacco Products; Apparel, Leather & Allied Products; Wood Products; Paper Products; Chemical Products; Computer & Electronic Products; Primary Metals; Miscellaneous Manufacturing; and Plastics & Rubber Products. Conversely, six industries reporting contraction include Petroleum & Coal Products; Textile Mills; Transportation Equipment; Furniture & Related Products; Fabricated Metal Products; and Machinery.

What Industry Professionals Are Saying

• “COVID-19 is impacting China’s raw material supply chain. We are now seeing revenue impact in that region. Our operations team is reviewing plans for spread of the virus.” (Computer & Electronic Products)

• “The two main issues affecting our business [are] COVID-19 and the oil-price war. We are in daily discussions and meeting constantly, updating tracking logs to document high risk concerns.” (Chemical Products)

• “COVID-19 impact has extended to Europe and North America. The virus escalation is affecting our purchasing and logistics operations. We have incurred air-shipment and production interruptions due to shortages of raw materials and components.” (Transportation Equipment)

• “We are experiencing a record number of orders due to COVID-19.” (Food, Beverage & Tobacco Products)

• “World demand for petroleum products is declining, while supply is ramping up. We have lost supply chain visibility to certain locations.” (Petroleum & Coal Products)

• “COVID-19’s spread in the U.S. may start impacting our domestic business. As for Asian suppliers, they are starting to get back up to speed.” (Fabricated Metal Products)

• “COVID-19 has caused a 30% reduction in productivity in our factory.” (Machinery)

• “A big part of our business is hospitality, and we are seeing demand drop and an increase in cancellations.” (Nonmetallic Mineral Products)

• “All North American manufacturing plants have ceased operations or drastically scaled back as a result of customer plant closings and other responses to COVID-19.” (Plastics & Rubber Products)

• “Volumes are down 4.3%, and some areas of the supply chain are being affected by the coronavirus.” (Furniture & Related Products)

Commodities Up in Price: Capacitors (2); Circuit Card Assemblies; Isopropyl Alcohol; Personal Protective Equipment (PPE)—Gloves; Resistors (2); Steel—Hot Rolled* (5); and Steel Products (2)

Commodities Down in Price: Aluminum (2); Aluminum Products (3); Base Oils; Copper (2); Corrugate (2); Crude Oil (2); Diesel Fuel; Fuel; Heating Oil; Natural Gas (4); Oil Products; Plastic; Scrap (2); and Steel—Hot Rolled* (2)

Commodities in Short Supply: Cleaning Wipes; Hand Sanitizer; Isopropyl Alcohol; Paper Towels; Personal Protective Equipment (PPE)—Gloves; PPE—Masks; and Toilet Paper

Note: The number of consecutive months the commodity is listed is indicated after each item. *Indicates both up and down in price.

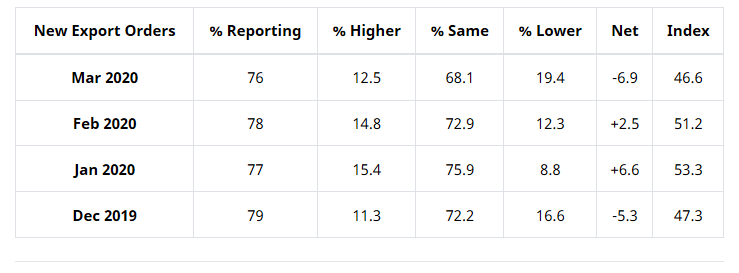

New Export Orders*

ISM®’s New Export Orders Index registered 46.6% in March, a decrease of 4.6 percentage points compared to the February reading of 51.2%. “The New Export Orders Index fell back into contraction territory after two consecutive months of growth. Only one of the six big industry sectors expanded during the period, down from three the previous month,” explained Fiore.

Four industries reported growth in new export orders during March: Apparel, Leather & Allied Products; Paper Products; Chemical Products; and Miscellaneous Manufacturing. Six industries reported a decrease in new export orders, including Transportation Equipment; Fabricated Metal Products; Machinery; Plastics & Rubber Products; Food, Beverage & Tobacco Products; and Computer & Electronic Products. Seven industries reported no change in exports in March compared to February.

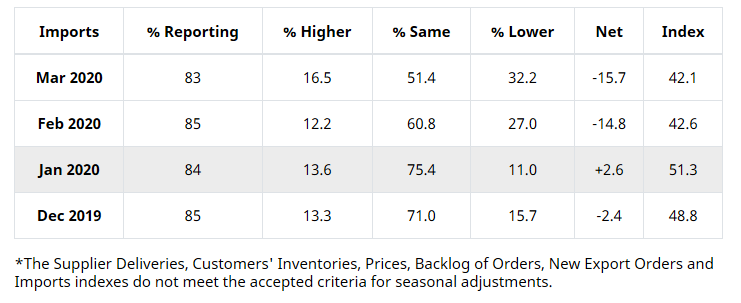

Imports*

ISM®’s Imports Index registered 42.1% in March, a decrease of 0.5 percentage point compared to the 42.6% reported during February. “For the second consecutive month, imports were in contraction territory, at levels not seen since the summer of 2009. As was the case in the Supplier Deliveries Index comments, respondents indicated the coronavirus as the primary cause of reduced import activity,” said Fiore.

Four industries reported growth in imports during March: Wood Products; Nonmetallic Mineral Products; Food, Beverage & Tobacco Products; and Chemical Products. Eleven industries reported a decrease in imports: Paper Products; Apparel, Leather & Allied Products; Primary Metals; Petroleum & Coal Products; Transportation Equipment; Machinery; Furniture & Related Products; Computer & Electronic Products; Electrical Equipment, Appliances & Components; Miscellaneous Manufacturing; and Fabricated Metal Products.