KPI – January 2024: Recent Vehicle Recalls

KPI – January 2024: State of Manufacturing

KPI – January 2024: State of the Economy

KPI – January 2024: Consumer Trends

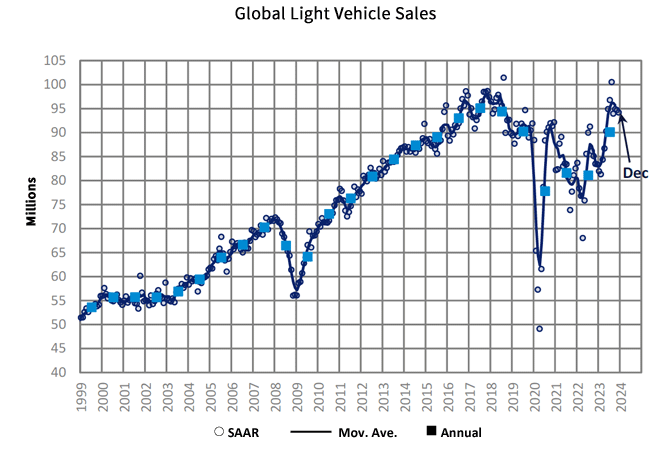

GLOBAL LIGHT VEHICLE SALES

In December, the Global Light Vehicle (LV) selling rate was 94 million units per year. The light vehicle market finished on a strong note, jumping 11.6% year-over-year to 8.4 million units in December.

The U.S. received a boost in sales thanks to year-end discounts and higher incentives offered by automakers. While Western Europe reached 13.3 million units in 2023, a 14.1% year-over-year increase, its light vehicle market in December proved lackluster, down 4.3%. In China, total light vehicles sales were up nearly 11% in 2023, with sales benefitting from stronger competition and aggressive price cuts.

“The current state of the global auto industry is healthy and near-term risks are down slightly from earlier in 2023. (Last) year is projected to finish at 89.6 million units, an 11% year-over-year increase,” said Jeff Schuster, group head and executive vice president of automotive at GlobalData. “In 2024, supply is expected to be sufficient for global demand growth of 3% to 92.3 million units. However, the outlook is not without risks. Most major markets are still dealing with high vehicle prices and there remains a risk of recession in North America and Europe. Next year is pivotal for manufacturers and may be the first true test for where natural demand is.”

Image Source: GlobalData Global Light Vehicle Sales Update (December 2023) – MarkLines Automotive Industry Portal

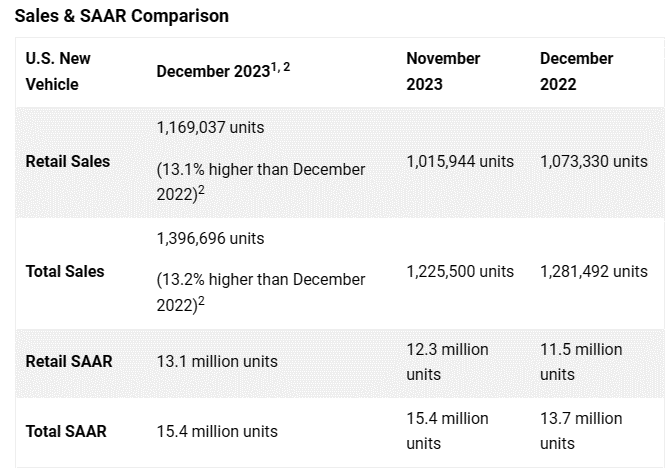

U.S. NEW VEHICLE SALES

Total new-vehicle sales for December 2023, including retail and non-retail transactions, are projected to reach 1,396,700 units – a 13.2% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

“December results cap off the year with a strong performance, illustrated by double-digit year-over-year sales growth and the second-highest consumer expenditure on new vehicles ever recorded for the month,” says Thomas King, president of the data and analytics division at J.D. Power.

“What’s even more noteworthy is that consumer expenditure on new vehicles in 2023 set a record of $578 billion. This is the third consecutive year in which U.S. consumers spent more than half a trillion dollars buying new vehicles,” he continues.

Important Takeaways, Courtesy of J.D. Power:

- Retail buyers are on pace to spend $50.4 billion on new vehicles, up $2.4 billion year-over-year.

- Trucks/SUVs are expected to account for 81% of new vehicle retail sales in December.

- The average new vehicle retail transaction price is estimated to reach $46,055, down $1,274 year-over-year.

- Average incentive spending per unit is expected to hit $2,458, up from $1,289 last year.

- Average interest rates for new-vehicle loans are predicted to increase to 6.9%, 46 basis points higher than a year ago.

- The total retailer profit per unit, which includes vehicles gross plus finance and insurance income, is estimated to be $2,729 in December.

- Fleet sales are expected to total 227,660 units in December, up 13.6% year-over-year on a selling day adjusted basis. Fleet volume will account for approximately 16.3% of total light-vehicle sales, unchanged from a year ago.

“In 2024, retail inventory is expected to keep rising and that increase in supply will lead to moderation in pricing. Additionally, anticipated interest rate cuts will also help affordability. This trend will drive an increase in sales, but at the expense of OEM and retailer per-unit profitability. This tradeoff between increased volume and lower per-unit profit means that total profitability for OEMs and retailers will remain very strong relative to historical levels,” King says.

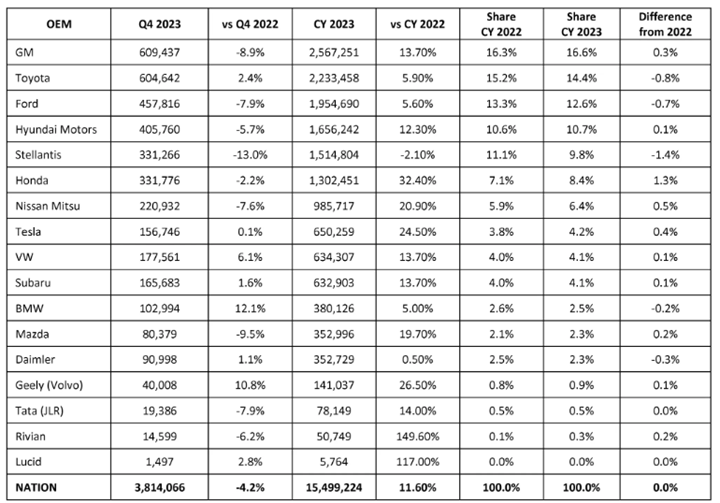

Review comprehensive 2023 year-end data, courtesy of Cox Automotive.

U.S. USED MARKET

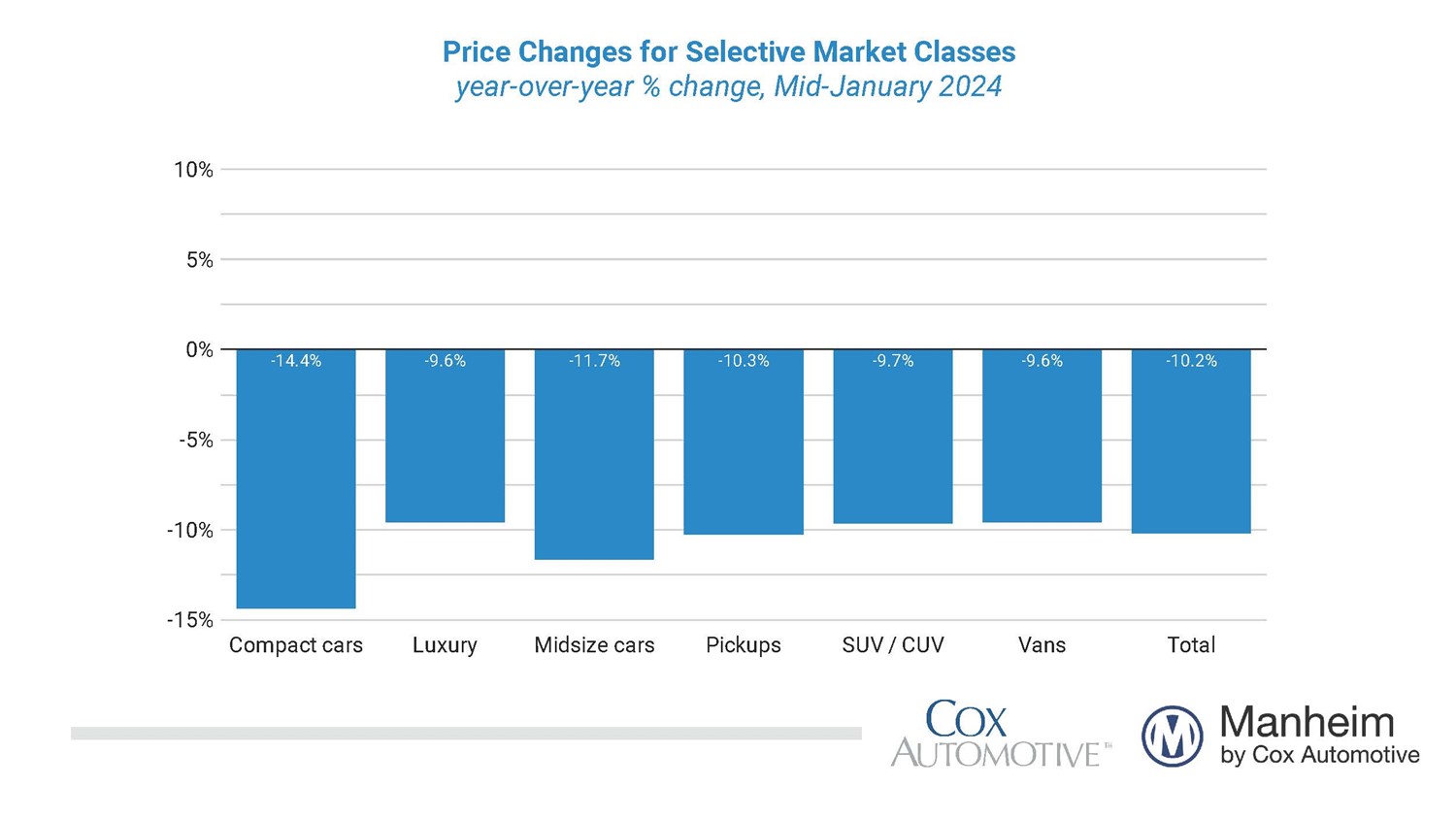

Wholesale used-vehicle prices (on a mix-, mileage- and seasonally adjusted basis) decreased 1% from December during the first 15 days of January. The mid-month Manheim Used Vehicle Value Index dropped to 201.9 – down 10.2% from the full month of January 2023.

According to Manheim, all major market segments posted seasonally adjusted prices that remained lower year-over-year in the first half of January. Compared to the industry’s 10.2% decline, SUVs dipped less at 9.7%, while luxury and vans both decreased 9.6%. Compact cars, mid-size cars and pickups were down 14.4%, 11.7% and 10.3% year-over-year, respectively.

All major segments posted negative price performance compared to December. Luxury vehicles, SUVs and compact cars were down 1.4%, 1.3 % and 1.1%, respectively. Midsize cars, pickups and vans declined 0.8%, 0.6% and 0.3%, respectively.

Overall, used-vehicle prices experienced a modest drop from the previous year but remain relatively close to their historical peak levels. For example, J.D. Power says the average trade-in equity is trending toward $8,521, down $780 from a year ago but nearly double the amount of pre-pandemic levels.

“The used-vehicle market is expected to regain some normalcy and balance in 2024,” added Chris Frey, senior manager of economic and industry insights at sister company Cox Automotive. “However, the effects of lower new-vehicle sales in 2021 and 2022 are anticipated to keep the used supply constrained.”