KPI – November 2023: State of the Economy

KPI – November 2023: State of Manufacturing

KPI – November 2023: State of Business – Automotive Industry

KPI – November 2023: Consumer Trends

Consumer confidence and sentiment continued to decline in October, with political tension, inflation, interest rates, labor challenges and war spooking small businesses and consumers alike.

The Conference Board Consumer Confidence Index declined moderately to 102.6 (1985=100) in October, down from an upwardly revised 104.3 in September. The Present Situation Index–based on consumers’ assessment of current business and labor market conditions–declined to 143.1 (1985=100) from 146.2.

The Expectations Index–based on consumers’ short-term outlook for income, business and labor market conditions–also fell slightly to 75.6 (1985=100) after declining to 76.4 in September.

The Expectations index remains below 80–a level which historically signals a recession within the next year. Consumer fears of an impending recession are elevated, consistent with the short and shallow economic contraction anticipated during the first half of 2024.

Similarly, the University of Michigan Survey of Consumers–a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions–dropped to 63.8 in October, a 5% month-over-month decline.

Moreover, November preliminary data projects a sharp downward trend to 60.4.

“Overall, lower-income and younger consumers exhibited the strongest declines in sentiment,” affirms Joanne Hsu, director of the University of Michigan’s Surveys of Consumers.

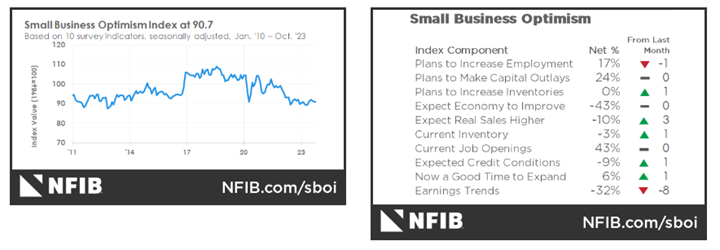

Small businesses continue to feel pessimistic about current conditions as well. According to the current NFIB Small Business Optimism Index, 22% of owners said inflation is the single most important problem in operating their business. As a result, 30% reported raising average selling prices–up another point month-over-month.

Overall, 61% of owners reported hiring or trying to hire in October, with 90% of owners reporting “few or no qualified applicants” for the positions they were trying to fill. Approximately 37% have openings for skilled workers and 18% have openings for unskilled labor. The difficulty in filling open positions is particularly acute in the transportation, construction and services sectors.

“The October data shows that small businesses are still recovering, and owners are not optimistic about better business conditions. Small business owners are not growing their inventories, as labor and energy costs are not falling–making it a gloomy outlook for the remainder of the year,” says Bill Dunkelberg, chief economist at NFIB.

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report:

TOP TAKEAWAYS:

- Economic activity in the manufacturing sector contracted in October for the 12th consecutive month following a 28-month period of growth, say the nation’s supply executives in the latest Manufacturing ISM Report On Business. The Manufacturing PMI registered 46.7% in October, 2.3 percentage points lower than the 49% recorded in September.

- In October, the Consumer Price Index for All Urban Consumers (CPI-U) was unchanged on a seasonally adjusted basis, says the U.S. Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 3.2% before seasonal adjustment.

- The NFIB Small Business Optimism Index dipped another 0.1 points in October (90.7), marking the 22nd month below the 50-year average of 98.

- Total new vehicle sales for October 2023, including retail and non-retail transactions, are projected to reach 1,201,800 units–a 6.6% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

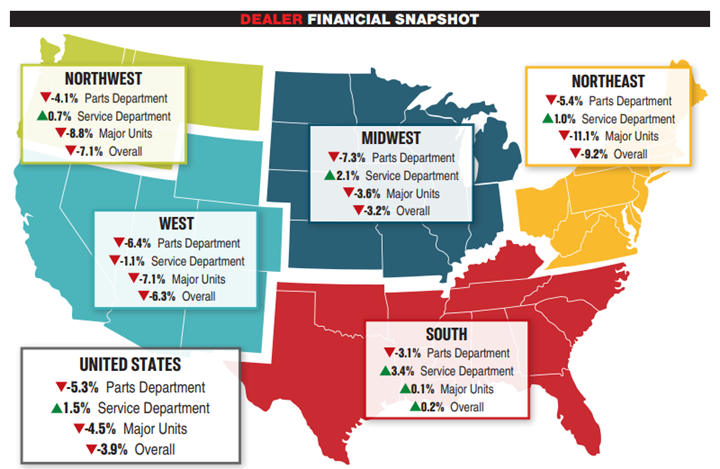

- Powersports Business says dealers across the country reported an overall revenue decline of 3.9% in September, according to composite data from more than 1,700 dealerships in the U.S. that utilize CDK Lightspeed DMS. On average, dealerships were down 4.5% in major units and 5.3% in the parts department. Even though service sales rose 1.5%, it was not enough to stave off the dip.