More than 590 million COVID-19 cases and 6.4 million deaths are confirmed across the globe. Vaccination efforts remain a top priority among health and government officials, with an ultimate goal of reaching herd immunity. Approximately 67% of Americans are fully vaccinated, according to recent CDC data. Experts estimate 70%-85% of the population must be vaccinated in order to reach herd immunity.

To date, nearly 93 million cases were reported across the U.S, with California, Texas and Florida claiming the highest numbers, according to Statista. COVID-19 restrictions vary by state, county and even city. Review a comprehensive list of current restrictions here.

COVID-19 Cases by Country

The Conference Board Consumer Confidence Index® decreased in July, following a significant decline in June. The Index now stands at 95.7 (1985=100), down 2.7 points from 98.4 in June. The Present Situation Index –based on consumers’ assessment of current business and labor market conditions – fell to 141.3 from 147.2 last month. The Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – ticked down to 65.3 from 65.8.

The Consumer Sentiment Index – a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions – increased slightly month-over-month to 55.1 from 51.5, according to the University of Michigan Survey of Consumers. Last month was the lowest reading on record, inclusive of consumers across income, age, education, geographic region, political affiliation, stockholding and homeownership status.

Inflation remains a primary concern to consumers, with 48% blaming inflation for eroding their living standards. High income consumers, who generate a disproportionate share of spending, registered large declines in both their current personal finances as well as buying conditions for durables.

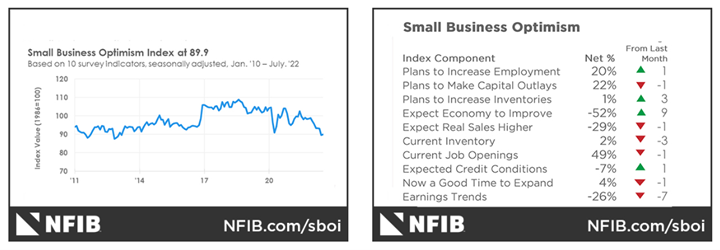

While the NFIB Small Business Optimism Index rose .4 points in July to 89.9, it marks the sixth consecutive month below the 48-year average of 98. Moreover, 37% of small business owners reported inflation as their “single most important problem” in operating their business, an increase of three points from June and the highest level since the fourth quarter of 1979.

“The uncertainty in the small business sector is climbing again as owners continue to manage historic inflation, labor shortages and supply chain disruptions,” says Bill Dunkelberg, NFIB chief economist. “As we move into the second half of 2022, owners will continue to manage their businesses into a very uncertain future.”

Key Data Points, Courtesy of NFIB:

- Owners expecting better business conditions over the next six months increased nine points from June’s record low level to a net-negative 52%, albeit the Uncertainty Index increased 12 points from last month to 67.

- Seasonally adjusted, a net 37% plan price hikes – down 12 points.

- Nine percent of owners cited labor costs as their top business problem and 21% said that labor quality was their top business problem, remaining in second place behind inflation.

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report:

This Month’s Top Takeaways:

- The July Manufacturing PMI® registered 52.8%, down 0.2 percentage point from a reading of 53% in June, according to supply executives in the latest Manufacturing ISM® Report On Business®.

- The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in July on a seasonally adjusted basis after rising 1.3% in June, notes the U.S. Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 8.5% before seasonal adjustment.

- LMC Automotive reports Global Light Vehicle (LV) sales improved to 90 million units per year in July but remains down 6.4% year-over-year. While China continues to recover and spur an increased global selling rate, other major markets are hamstrung by ongoing conflict in Ukraine.

- Total new vehicle sales for July 2022, including retail and non-retail transactions, are projected to reach 1,159,700 units – a 5.7% decrease from July 2021, according to a joint forecast from D. Power and LMC Automotive.

- The RV industry continues to post record numbers, with RV wholesale shipments projected to exceed 549,000 units by year-end 2022, according to the Summer 2022 issue of RV RoadSigns, the quarterly forecast prepared by ITR Economics for the RV Industry Association (RVIA).

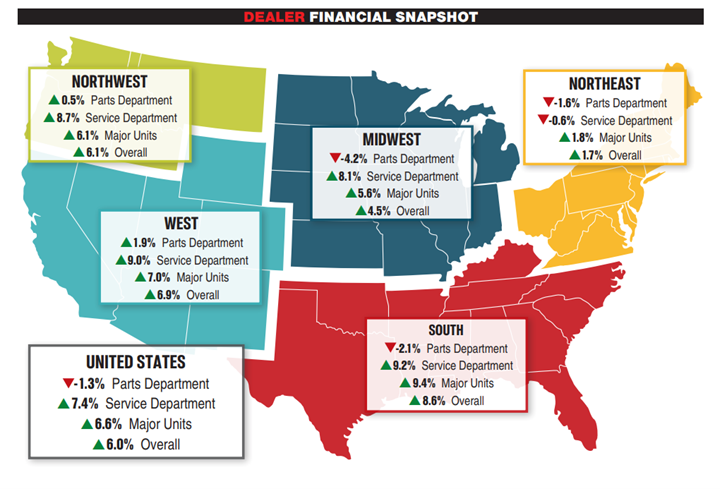

- Powersports Business reports dealerships across the country, on average, posted year-over-year revenue growth in June. Revenue from sales of new and pre-owned units rose by an average of 6.6%, with the South (9.4% growth) and the West 7% growth) providing especially notable increases month-over-month versus year-over-year. The service department saw a 7.4% bump, with every region except the Northeast performing above an 8% increase. The Northeast region was down 0.6% in service revenue. Parts sales declined 1.3% year-over-year on average, a noticeably better percentage than May 2021 (2.9% decrease) and April 2021 (6.1% decrease). The Midwest saw the greatest decrease in parts revenue with a 4.2% decline. The West (1.9% growth) and the Northwest (0.5% growth) regions saw the greatest increase in parts revenue. Combined, the average dealership experienced an overall revenue increase of 6% in June, a considerable gain compared to the 2.6% increase in May 2022. The South posted the largest overall revenue increase at 8.6% and the West followed with a 6.9% increase.