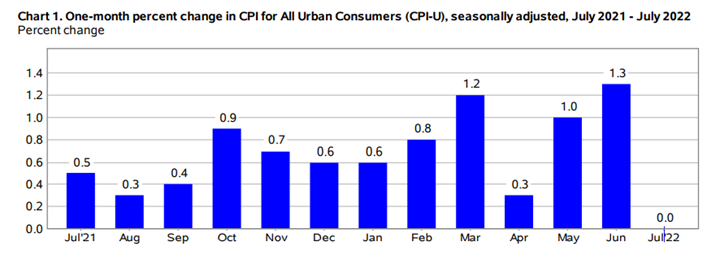

The Consumer Price Index for All Urban Consumers (CPI-U) was unchanged in July on a seasonally adjusted basis after rising 1.3% in June, according to the U.S. Bureau of Labor Statistics. Over the last 12 months, the all-items index increased 8.5% before seasonal adjustment.

The gasoline index fell 7.7% in July, effectively offsetting increases in the food and shelter indexes. This led to the all-items index remaining unchanged month-over-month. While the energy index fell 4.6% as the indexes for gasoline and natural gas declined, the index for electricity increased. Meanwhile, the food and food-at-home indexes continued to rise, increasing another 1.1% and 1.3%, respectively.

The indexes for shelter, medical care, motor vehicle insurance, household furnishings and operations, new vehicles and recreation were among those that increased month-over-month. There were some indexes that declined in July, including airline fares, used cars and trucks, communication and apparel.

The all-items index increased 8.5% for the 12 months ending July, while the all items less food and energy index rose 5.9% over the last 12 months. The energy index increased 32.9% for the 12 months ending July, a smaller increase than the 41.6% increase for the period ending June. The food index increased 10.9% over the last year, the largest 12-month increase since the period ending May 1979.

“Our work here is far from done. I cannot underscore that enough,” says Jared Bernstein, White House Council of Economics Advisers member. “The president will continue to talk about unacceptably high inflation.”

Employment

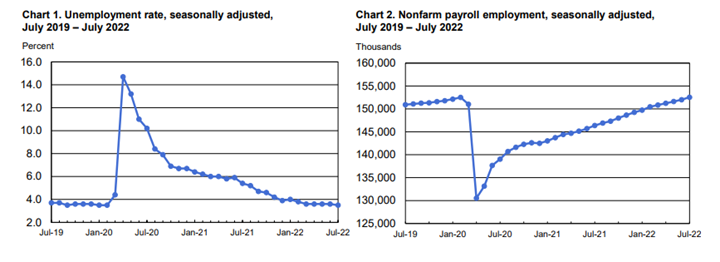

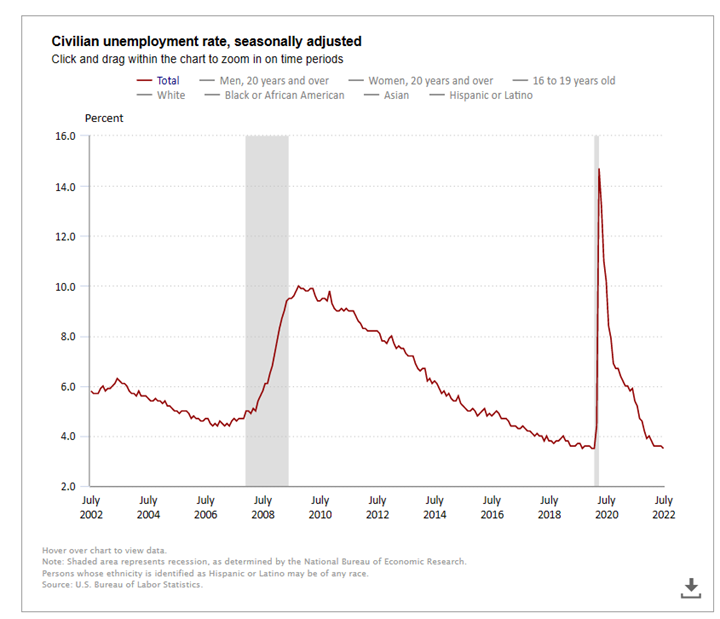

Total nonfarm payroll employment rose by 528,000 in July, while the unemployment rate edged down to 3.5%. “The report throws cold water on a significant cooling in labor demand [and] is a good sign for the broader U.S. economy and worker,” says Bank of America economist Michael Gapen.

Important Takeaways, Courtesy of the Bureau of Labor Statistics:

- The number of persons on temporary layoff (791,000) changed little month-over-month and essentially returned to its pre-pandemic level.

- Among the unemployed, the number of permanent job losers sits at 1.2 million. The figure continues to trend down, currently 129,000 lower than in February 2020.

- The number of long-term unemployed (those jobless for 27 weeks or more) decreased by 269,000 in July to 1.1 million. This measure returned to its February 2020 level. The long-term unemployed accounted for 18.9% of the total unemployed in July.

Bank of America says its proprietary measures of labor market momentum show an employment picture that is strong but slowing, due in large part to central bank policy tightening. The Fed raised benchmark interest rates four times this year – totaling 2.25 percentage points and bringing the federal funds rate to its highest level since December 2018.

Meanwhile, gross domestic product – the measure of all goods and services produced – declined the first two quarters of 2022, thereby meeting a common definition of a recession.

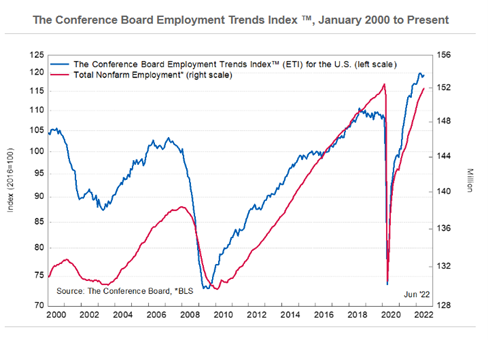

“While the US labor market is currently still robust, the recent behavior of the Index signals that slower job gains should be expected over the next several months. This would bring the labor market in line with the rest of the economy, where economic activity already has been slowing,” says Frank Steemers, senior economist at The Conference Board.

“It is increasingly likely that the U.S. economy will fall into recession by year-end or early 2023, with the Fed expected to continue raising interest rates rapidly over the coming months. While businesses are currently still struggling with severe labor shortages, they may soon see some reduced pressure in recruitment and retention difficulties as economic activity cools. Depending on the severity of the recession, some months of negative jobs growth are possible over the year ahead,” adds Steemers.

The Conference Board expects the unemployment rate – just 3.5% as of July 2022 – to remain below 4.5% in 2023.

The Conference Board Employment Trends Index™ (ETI) decreased in July 2022 to 117.63—down from a downwardly revised 118.71 in June.

By Demographic

Unemployment rates among the major worker groups: adult women – 3.1%; adult men – 3.2%; teenagers – 11.5%; Asians – 2.6%; Whites – 3.1%; Hispanics – 3.9%; and Blacks – 6%.

By Industry

Total nonfarm payroll employment racked up 528,000 in July, notably larger than the average monthly gain over the prior four months (+388,000). Job growth was widespread, led by gains in leisure and hospitality, professional and business services and health care.

Total nonfarm employment increased by 22 million since reaching a low in April 2020, thus returning to its pre-pandemic level. Private-sector employment is 629,000 higher than in February 2020, although several sectors have yet to recover. Government employment is 597,000 lower than its pre-pandemic level.

Important Takeaways, Courtesy of the U.S. Bureau of Labor Statistics:

- Employment in leisure and hospitality added 96,000 jobs, as growth continued in food services and drinking places (+74,000). However, employment in leisure and hospitality is below its February 2020 level by 1.2 million, or 7.1%.

- Employment in professional and business services continued to grow, with an increase of 89,000 in July. Job growth was widespread within the industry, including gains in management of companies and enterprises (+13,000), architectural and engineering services (+13,000), management and technical consulting services (+12,000) and scientific research and development services (+10,000). Employment in professional and business services is 986,000 higher than in February 2020.

- Manufacturing employment increased by 30,000. Employment in durable goods industries rose by 21,000, with job gains in semiconductors and electronic components (+4,000) and miscellaneous durable goods manufacturing (+4,000). Employment in manufacturing is 41,000 above its February 2020 level.

- Employment in construction increased by 32,000, as specialty trade contractors added 22,000 jobs. Construction employment is 82,000 higher than in February 2020.

“Currently, the labor market is still strong and labor shortages are severe. However, this picture could change towards the end of 2022 and early 2023,” says Steemers. “With inflation still elevated and the Fed expected to continue to raise interest rates rapidly, the risk of a short and mild recession is growing. In such a scenario, employers may reduce hiring – and possibly implement furloughs and layoffs, depending on the severity of a potential economic contraction. By early 2023, there could possibly be monthly job losses – and in that case, the unemployment rate would tick up.”

Review all employment statistics here.