- KPI – June 2025: The Brief

- KPI – June 2025: State of Manufacturing

- KPI – June 2025: State of Business – Automotive Industry

- KPI – June 2025: State of the Economy

- KPI – June 2025: Recent Vehicle Recalls

Below is a synopsis of consumer confidence, sentiment, demand and income/spending trends.

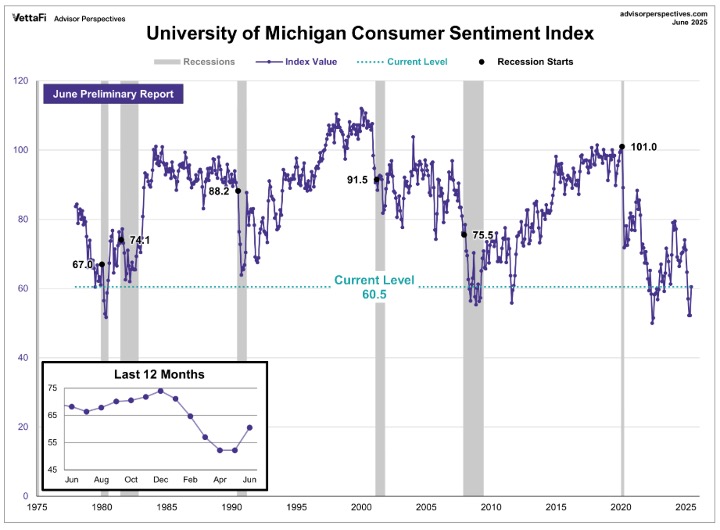

The University of Michigan Survey of Consumers—a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions—registered 52.2% in May and posted a preliminary reading of 60.5% in June.

Consumer sentiment improved for the first time in six months, climbing 16% from last month but approximately 20% below December 2024 levels when sentiment exhibited a post-election bump.

All five index components were on the rise, with a particularly steep increase in short and long-run expected business conditions, consistent with a perceived easing of pressures from tariffs. According to survey data, these collective trends were representative across age, income, wealth, political party and geographic region.

“Consumers appear to have settled somewhat from the shock of the extremely high tariffs announced in April and the policy volatility seen in the weeks that followed,” says Joanne Hsu, director of Survey of Consumers. “However, consumers still perceive wide-ranging downside risks to the economy. Their views of business conditions, personal finances, buying conditions for big ticket items, labor markets and stock markets all remain well below six months ago in December 2024.”

Despite this month’s notable improvement, Hsu says consumers remain “guarded and concerned” about the trajectory of the economy.

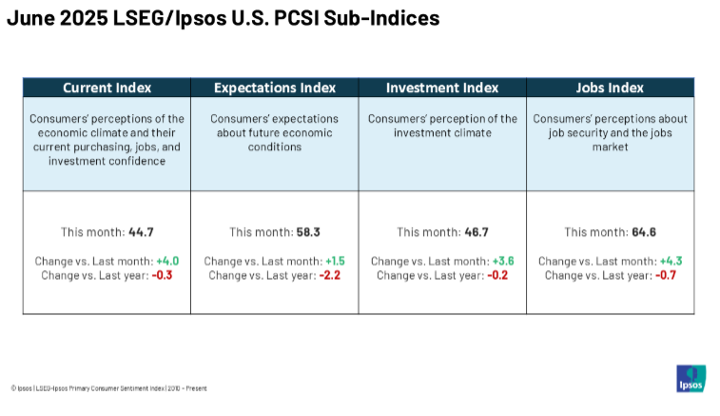

Caption: The LSEG/Ipsos Primary Consumer Sentiment Index for June 2025 is at 53.4. Fielded from May 23–June 5, 2025, the Index is up 3.4 points from last month.

Unlike Survey of Consumers, The Conference Board Consumer Confidence Index “deteriorated” by 5.4 points, dropping from 98.4 in May to 93.0 in June. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—fell 6.4 points to 129.1. Meanwhile, the Expectations Index—based on consumers’ short-term outlook for income, business and labor market conditions—declined 4.6 points to 69.0, substantially below the threshold of 80 that typically signals a recession ahead.

“Consumer confidence weakened in June, erasing almost half of May’s sharp gains,” says Stephanie Guichard, senior economist of global indicators at The Conference Board. “The decline was broad-based across components, with consumers’ assessments of the present situation and their expectations for the future both contributing to the deterioration. Consumers were less positive about current business conditions than May. Their appraisal of current job availability weakened for the sixth consecutive month but remained in positive territory, in line with the still-solid labor market.”

“Consumers were more pessimistic about business conditions and job availability over the next six months, and optimism about future income prospects eroded slightly,” she continues.

Key Takeaways, Courtesy of The Conference Board:

- June’s “retreat in confidence” was representative of all age groups and almost all income groups. It was also shared across all political affiliations, with the largest decline among Republicans.

- Consumers’ outlook on stock prices continued to recover from April’s 16-month low, with 45.6% expecting stock prices to increase over the next 12 months in June, up from 37.6% two months ago. Nearly 57% of those surveyed expected rates to rise, the highest share since October 2023.

- Compared to May, purchasing plans for cars were steady at the highest level since December 2024, while purchasing plans for homes declined. More consumers were undecided about plans to buy big-ticket items overall. Buying plans for most appliances were slightly up, while plans to buy electronics goods were down. Consumers’ intentions to purchase more services in the months ahead weakened compared to May, with almost all services categories declining. Dining out remained a shining star among spending intentions in services. It was one of the few categories to see spending intentions rise in June, along with motor vehicle services, museum/historic sites and fitness. Vacation intentions were unchanged. More consumers planned to travel abroad, while intentions to travel in the U.S. declined.

- Consumers’ views of their Family’s Current Financial Situation remained “solid” but dipped slightly. Consumers’ expectations regarding their Family’s Future Financial Situation improved to a four-month high. The share of consumers expecting a recession over the next 12 months rose slightly and remained above the levels seen in 2024.

According to Guichard, consumers’ write-in responses revealed little change in the top issues impacting their views of the economy.

“Tariffs remained on top of consumers’ minds and were frequently associated with concerns about their negative impacts on the economy and prices. Inflation and high prices were another important concern cited by consumers in June. However, there were a few more mentions of easing inflation compared to last month. This is in line with a cooling in consumers’ average 12-month inflation expectations to 6.0% (down from 6.4% in May and 7% in April),” she says. “References to geopolitics and social unrest increased slightly from previous months but remained much lower on the list of topics affecting consumers’ views.”

Consumer Income & Spending

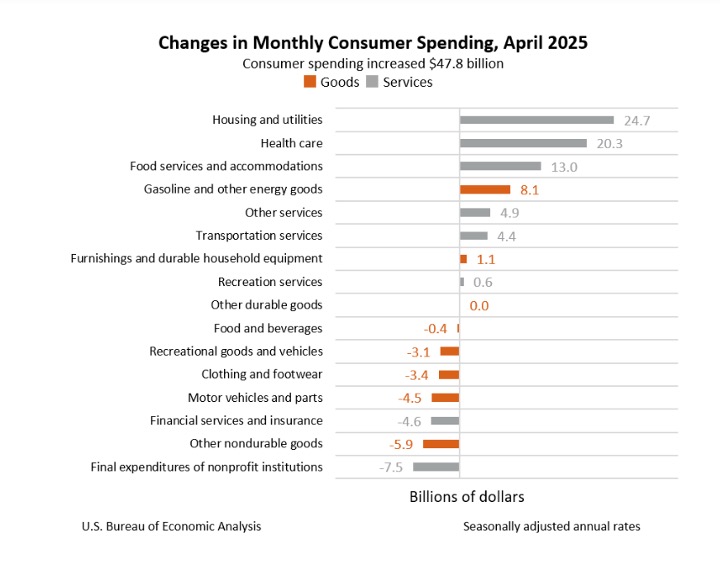

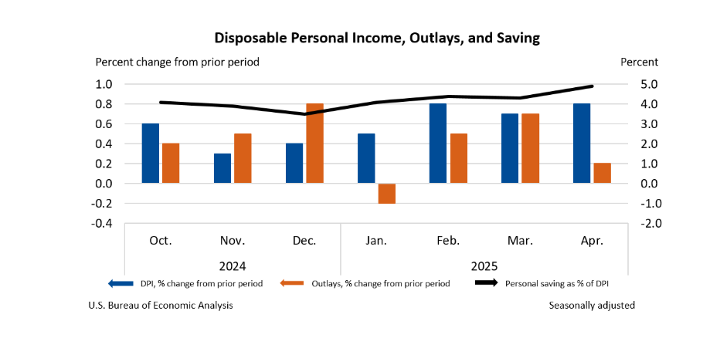

According to the U.S. Bureau of Economic Analysis (BEA), personal income increased $210.1 billion (0.8% at a monthly rate) during April 2025. Disposable personal income (DPI)—personal income less personal current taxes—increased $189.4 billion (0.8%), while personal consumption expenditures (PCE) increased $47.8 billion (0.2%).

Personal outlays—the sum of PCE, personal interest payments and personal current transfer payments—increased $48.6 billion in April. Personal saving was $1.12 trillion and the personal saving rate—personal saving as a percentage of disposable personal income—registered 4.9%.

Important Takeaways, Courtesy of BEA:

- In April, the $47.8 billion increase in current-dollar PCE reflected an increase of $55.8 billion in spending on services that was partly offset by a decrease of $8 billion in spending for goods.

- Compared to the preceding month, the PCE price index increased 0.1%. Excluding food and energy, the PCE price index also increased 0.1%.

- The PCE price index increased 2.1% year-over-year. Excluding food and energy, the PCE price index increased 2.5% from one year ago.