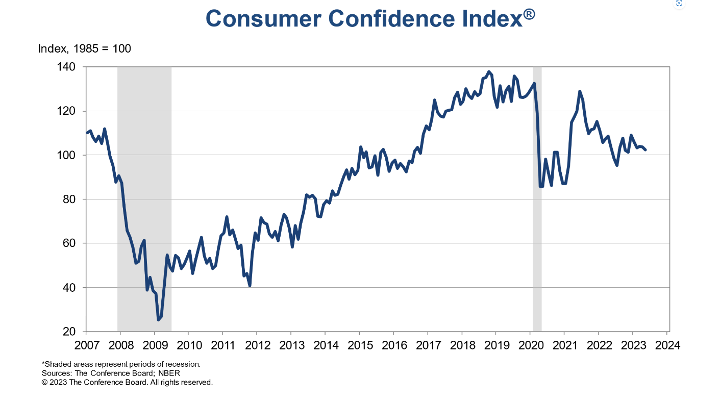

The Conference Board Consumer Confidence Index® declined to 102.3 (1985=100) in May, down from an upwardly revised 103.7 in April. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – decreased to 148.6 (1985=100) from 151.8 last month. The Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – dipped slightly to 71.5 (1985=100) from 71.7. For context, the Expectations Index has been below 80 since February 2022 (with the exception of a brief uptick in December 2022) – a level which often signals recessionary times.

According to recent data, while consumer confidence dipped across all age and income categories over the past three months, May’s decline reflects a “particularly notable worsening” among consumers aged 55-plus. Consumer assessment of current employment conditions proved the most significant deterioration, with the proportion of consumers reporting jobs are “plentiful” falling from 47.5% in April to 43.5% in May. While consumers expressed a more “downbeat” outlook regarding future business conditions, expectations for jobs and incomes over the next six months held relatively steady.

The Conference Board Consumer Confidence Index® indicates consumers may be showing signs of “pulling back spending” in the face of persistently high prices and rising interest rates. Recent data shows consumers are cautious in purchasing appliances, vehicles, homes and even vacations. According to Ataman Ozyildirim, senior director at The Conference Board, current times may signal consumers are “economizing amid growing pessimism.”

The chart evaluates the historical context for this index as a coincident indicator of the economy. Toward this end, Advisor Perspectives highlighted recessions and included GDP. To put the current data into better perspective, professionals state consumer sentiment is 30.5% below its average reading (arithmetic mean) and 29.6% below its geometric mean. The current index level is at the 3rd percentile of the 545 monthly data points in this series. This indicator is somewhat volatile, with a 3.1- point absolute average monthly change. The latest data point saw a 4.3-point decrease from the previous month.

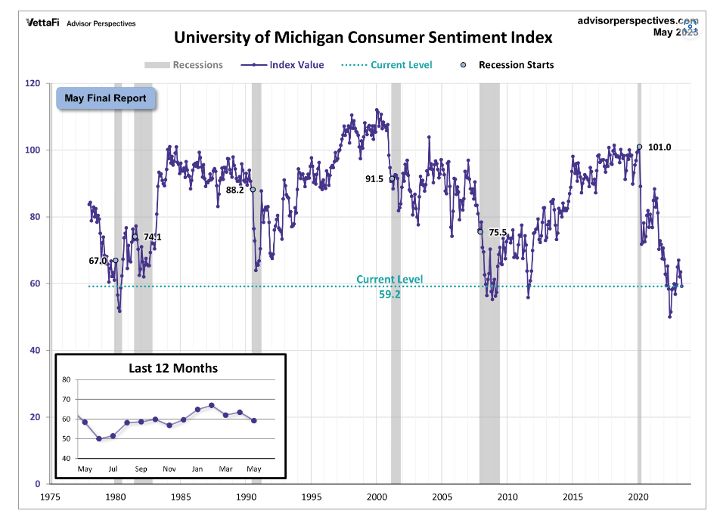

Similarly, the University of Michigan Survey of Consumers – a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions – registered 59.2 in May, a 7.7% month-over-month decline.

“Consumer resilience has been supported by strong incomes thus far. However, high inflation continues to erode consumers’ living standards and their confidence in the economy remains woefully negative,” says Joanne Hsu, director of Survey of Consumers.

Important Takeaways, Courtesy of Survey of Consumers:

- This month, sentiment fell severely for consumers in the West and those with middle incomes. The year-ahead economic outlook plummeted 17% from last month. Long-run expectations plunged by 13% as well, indicating that consumers are concerned any recession will bring lasting pain.

- Year-ahead inflation expectations receded to 4.2% in May after spiking to 4.6% in April.

- Uncertainty (as measured by the interquartile range of these expectations) remains elevated, averaging 7.8 over the last 12 months. However, it fell this month to 5.7, the lowest level of uncertainty in almost two years. This suggests that consumer views regarding short-run inflation may be stabilizing following four months of vacillation.

- Long-run inflation expectations inched up for the second straight month but remained within the narrow 2.9-3.1% range for 21 of the last 22 months.

“This decline mirrors the 2011 debt ceiling crisis, during which sentiment also plunged,” Hsu says. “That said, consumer views over their personal finances are little changed from April, with stable income expectations supporting consumer spending for the time being.”

Consumer Income & Spending

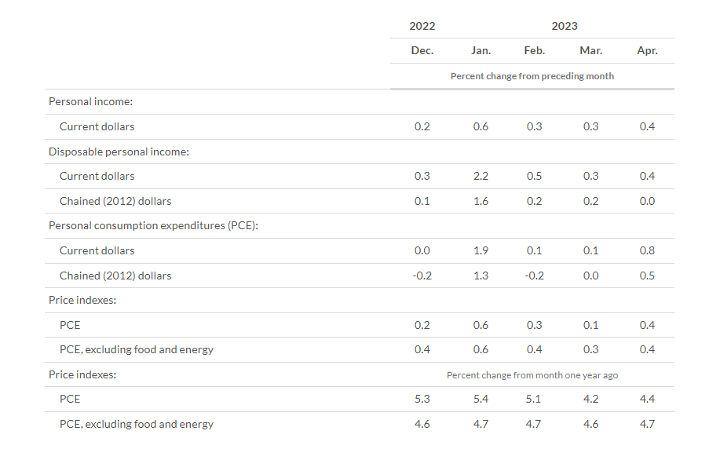

According to the U.S. Bureau of Economic Analysis (BEA), in April 2023 personal income increased $80.1 billion (0.4%), disposable personal income (DPI) increased $79.4 billion (0.4%) and personal consumption expenditures (PCE) increased $151.7 billion (0.8%).

In addition, personal outlays increased $156 billion in April. Personal saving was $802.1 billion and the personal saving rate – personal saving as a percentage of disposable personal income – was 4.1%.

Important Takeaways, Courtesy of BEA:

- In April, the $151.7 billion increase in current-dollar PCE reflected an increase of $86.9 billion in spending for services and a $64.8 billion in spending for goods. The largest contributors to the increase in services were financial services and insurance, health care and “other” services (notably professional and other services). Within goods, spending for motor vehicles and parts (led by new motor vehicles) and “other” nondurable goods (notably pharmaceutical products) were the largest contributors to the increase.

- The PCE price index increased 4.4% year-over-year in April. Prices for goods increased 2.1% and prices for services increased 5.5%. Food prices increased 6.9%, while energy prices decreased 6.3%. Excluding food and energy, the PCE price index increased 4.7% year-over-year.