- KPI – February 2026: The Brief

- KPI – February 2026: State of Manufacturing

- KPI – February 2026: State of the Economy

- KPI – February 2026: Consumer Trends

- KPI – February 2026: Recent Vehicle Recalls

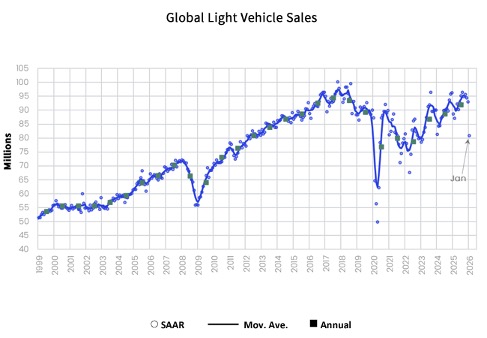

Global Light Vehicle Sales

In January, the Global Light Vehicle (LV) selling rate declined sharply to 81 million units per year due to a steep contraction in the Chinese PV market. The market decreased 2% year-over-year, as sales totaled 6.6 million units globally.

For the first time in an extended period, the U.S., Western Europe and China all experienced a dip in the same month, with drivers varying by region. In the U.S., severe weather weighed on sales, while the reduction in NEV purchase-tax discounts and changes to the trade-in subsidy program sharply reduced volumes in China. Meanwhile, a December pull-forward was followed by a muted start to 2026 in Western Europe.

According to GlobalData, February sales are expected to decrease 5.5% year-over-year. Once again, China is likely to be a major contributor to the loss, considering last year’s high baseline. On the contrary, India is likely to see strong growth in February, as tax reductions implemented in September 2025 continue to generate year-over-year gains. The global selling rate is expected to reach 89.3 million units in February.

“Our forecast for total global sales in 2026 stands at 93.5 million units, up 1.9% year-over-year. Our Chinese sales outlook has been revised down by around 300k units based on weaker momentum in the new year. Although China should still see some growth in 2026, developing markets such as India will also contribute significantly to the global expansion in light-vehicle sales this year, while most mature markets are expected to see a flat outcome or only modest gains,” says David Oakley, manager of Americas vehicle sales forecasts at GlobalData.

U.S. New Vehicle Market

Total new-vehicle sales for February 2026, including retail and non-retail transactions, are projected to reach 1,183,000—a 3.8% year-over-year decrease, according to a joint forecast from J.D. Power and GlobalData.

“As in January, performance is being shaped by depressed electric vehicle (EV) retail demand—EVs are expected to account for just 6.6% of retail sales, down 1.8 percentage points from a year ago—while elevated transaction prices continue to weigh on volumes through ongoing affordability pressure. Despite the relatively slow start to the year, acceleration in the sales pace is expected over the balance of 2026, starting with March, which is traditionally a high-volume sales month with elevated promotional activity from manufacturers,” says Thomas King, president of the data and analytics division at J.D. Power.

Key Takeaways, Courtesy of JD Power:

- Retail buyers are on pace to spend $41.3 billion on new vehicles, down $1 billion year-over-year.

- Internal combustion engine (ICE) vehicles are projected to account for 78.7% of new vehicle retail sales, an increase of 2.6 percentage points from a year ago. Hybrid electric vehicles (HEV) are expected to account for 13.5% of new vehicle retail sales, up 0.1 percentage points. EVs are expected to account for 6.6% of sales, down 1.8 percentage points, while plug-in hybrid vehicles (PHEV) are on pace to make up 1.1% of sales, down one percentage point year-over-year.

- Leasing is expected to account for 24.4% of sales this month, flat from a year ago.

- The average new vehicle retail transaction price is anticipated to reach $46,303, up $1,225 year-over-year.

- Average monthly finance payments are on pace to be $811, up $32 from last year.

- Total retailer profit per unit, which includes vehicle gross plus finance and insurance income, is expected to be $2,524, up $83 year-over-year and up $160 month-over-month. Total aggregate retailer profit from new vehicle sales is projected to be $2.3 billion this month, down 1.8% from last year.

- Fleet sales are expected to total 251,681 units in February, down 0.4% year-over-year. Fleet volume is expected to account for 21.3% of total light-vehicle sales, up 0.7 percentage points from a year ago.

“Looking ahead, multiple automakers have publicly stated their intent to increase their sales volume in 2026. However, given total new vehicle sales this year are expected to be similar to a year ago, and few, if any, automakers are planning for a sales contraction, competitive intensity can be expected to rise in the coming months,” King says.

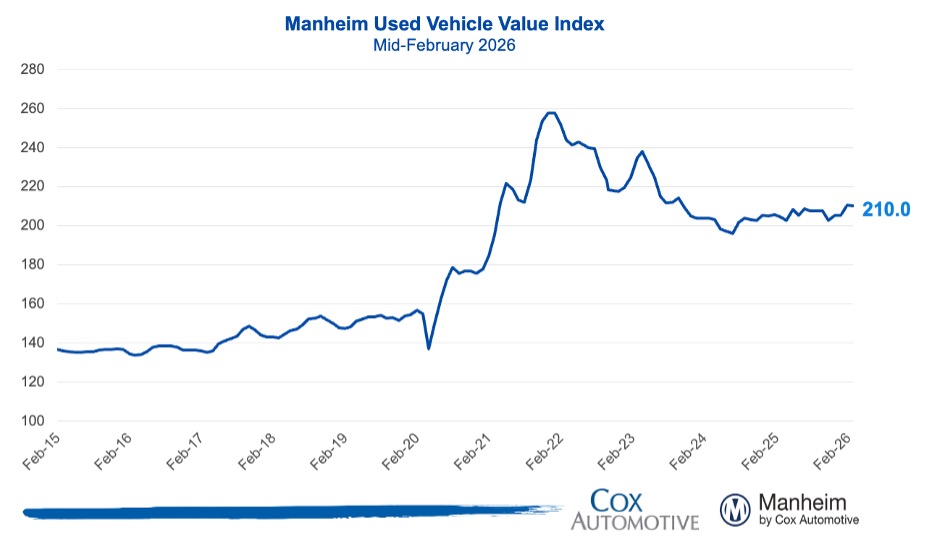

U.S. Used Market

The Manheim Used Vehicle Value Index (MUVVI) decreased to 210.0, reflecting a 0.2% decrease in wholesale used-vehicle prices (adjusted for mix, mileage and seasonality) during the first 15 days of February compared to January, and a 2.9% year-over-year increase. Seasonally adjusted wholesale values typically decrease by about 0.2% on average over the full month.

“The wholesale market carried its January momentum into February, with year-over-year price growth accelerating to 2.9% even as the seasonally adjusted index edged lower—a pattern consistent with the spring selling season getting an early start. Tax refund season is now in full swing, and the early data is encouraging: the average refund is up roughly 11% from this time last year, and the share of returns receiving a refund is up two percentage points,” says Jonathan Gregory, senior manager of economic and industry insights at Cox Automotive.

Data shows demand is already translating into sales conversion, climbing to 62.5% in the first half of February—up nearly three points year-over-year and 2.4 points from January, while MMR retention held above 100%.

“Dealers came into the month stocking up ahead of what many expect to be a strong spring, and the luxury segment continues to lead. We’re also seeing EV values firm up after some post-incentive softness earlier in the year. Wholesale supply has ticked up slightly to 28 days, but with conversion rates running this strong, that inventory is being absorbed. With lower auto loan rates giving more consumers the confidence to act and a potentially prolonged tax refund tailwind, wholesale values should find sustained support through the spring season,” Gregory says.

Click here to view results by segment.