KPI – February 2026: The Brief

KPI – February 2026: State of Manufacturing

KPI – February 2026: State of Business – Automotive Industry

KPI – February 2026: State of the Economy

KPI – February 2026: Recent Vehicle Recalls

Below is a synopsis of consumer sentiment, confidence, demand and income/spending trends.

Sentiment

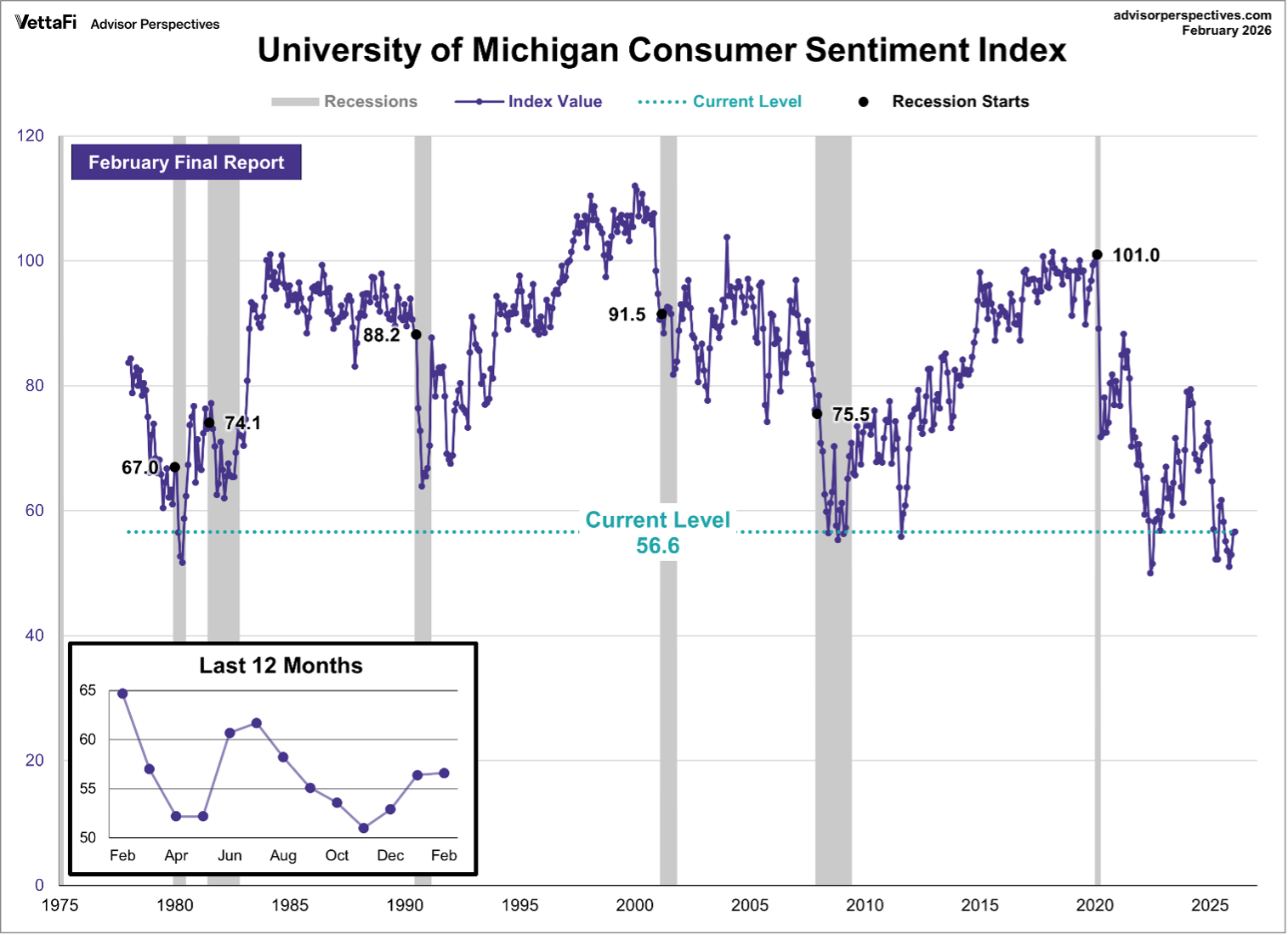

The University of Michigan Survey of Consumers – a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions – registered 56.4 in January and posted a preliminary reading of 56.6 in February.

While data shows consumer sentiment was stagnant month-over-month, approximately 46% of consumers “spontaneously mentioned” high prices eroding their personal finances. Readings have exceeded 40% for seven months in a row, according to Survey of Consumers.

“Sentiment is about 13% below a year ago and 21% below January 2025. That said, views vary considerably across the population. A sizable month-to-month increase in sentiment for the largest stockholders was fully offset by a decline among consumers without stock holdings,” says Joanne Hsu, director of Survey of Consumers. “Similar divergences were seen across income and education, where higher-income or college educated consumers exhibited increases in sentiment while lower-income or less-educated counterparts did not. With their much stronger income prospects and investment portfolios, wealthier and higher-income consumers feel better-insulated from any possible risks to the economy.”

Caption: To put this month’s report in historical context, consumer sentiment is currently 32.7% below its average reading of 84.0 (arithmetic mean) and 31.7% below its geometric mean of 82.8, based on data dating back to 1978.

Key takeaways, courtesy of Survey of Consumers:

- Year-ahead inflation expectations fell from 4% last month to 3.4% this month, the lowest reading since January 2025. This month’s reading still exceeds those seen in 2024 and remains well above the 2.3%-3% range seen in the two years pre-pandemic.

- Long-run inflation expectations held steady at 3.3%, just above the 2.8%-3.2% range seen in 2024. In 2019 and 2020, long-run inflation expectations were consistently below 2.8%. Uncertainty, as measured by the middle 50% of expectations, is now at its lowest since December 2024 for the short run and October 2024 for the long run.

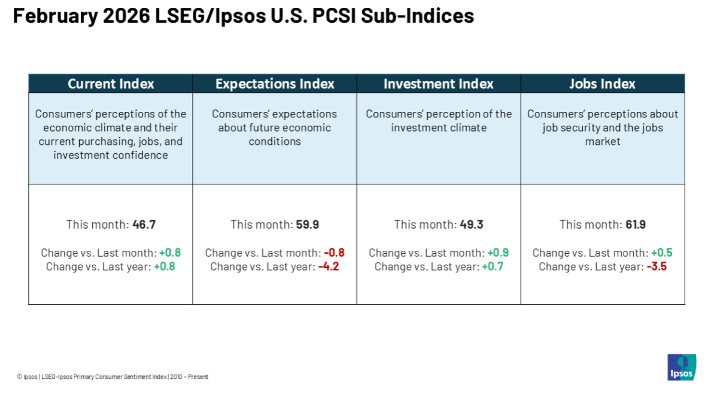

Caption: The LSEG/Ipsos Primary Consumer Sentiment Index for February 2026 is at 53.8. Fielded from Jan. 23-27, 2026, the Index is unchanged from the previous month.

Confidence

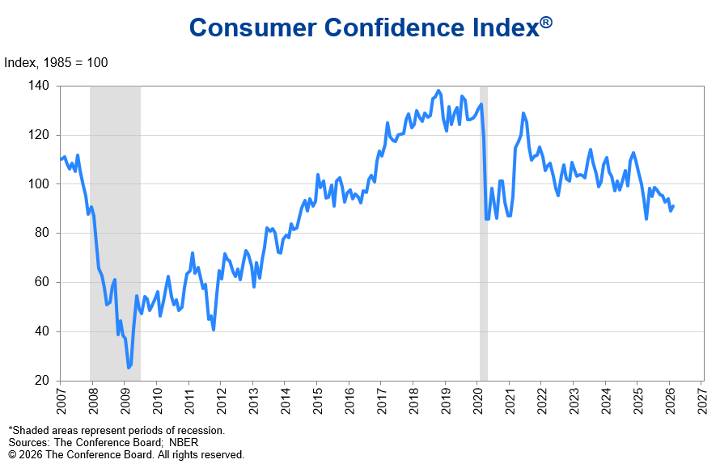

The Conference Board Consumer Confidence Index increased by 2.2 points, from an upwardly revised 89.0 in January to 91.2 in February. The Present Situation Index – based on consumers’ assessment of current business and labor market conditions – decreased by 1.8 points to 120.0 in February. Meanwhile, the Expectations Index – based on consumers’ short-term outlook for income, business and labor market conditions – rose by 4.8 points to 72.0.

“Confidence ticked up in February after falling in January, as consumers’ pessimistic expectations for the future eased somewhat,” says Dana Peterson, chief economist at The Conference Board. “Four-of-five components of the Index firmed. Nonetheless, the measure remained well below the four-year peak achieved in November 2024 (112.8).”

While confidence ticked up among consumers under age 35, it edged down for respondents 35 and older. On a six-month moving average basis, confidence among Generation Z rose, consistent with soundings from the under-age-35 group, but fell among other generations. Confidence continued to dip among most income brackets.

“Consumer confidence by political affiliation revived among Republican and Independent voters in February after a dip in January, while Democrats were less optimistic,” according to Peterson.

Key takeaways, courtesy of The Conference Board:

- Consumers’ average and median 12-month inflation expectations were little changed but remained elevated.

- Consumers also believed that interest rates will persist at higher levels over the next 12 months.

- Most consumers continued to expect stock prices to be higher 12 months from now, although the share was slightly smaller than last month.

- On net, consumers’ views of their Family’s Current Financial Situation retreated in February, after an unexpected surge in January, based on final data. Expectations for their Family’s Future Financial Situation continued to be less optimistic.

- The share of consumers who said a U.S. recession over the next 12 months is “very likely” fell, while those saying “not likely” rose. Respondents who said recession is “somewhat likely” over the next year increased somewhat, and the percentage believing we are “already in one” dipped.

- Consumers’ plans to buy big-ticket items over the next six months rose in February. Those who said “yes” and “maybe” to buying big-ticket items ahead increased, while the number of those saying “no” declined. Furniture, dishwashers, TVs and smartphones were the most popular items referenced.

- Buying plans for autos rose on a six-month moving average basis, continuing the upward trend in recent months. Consumers continued to prefer buying used cars. The share of consumers looking to buy a new car was unchanged. Homebuying expectations were little changed in February but continued to retreat on a six-month basis. Still, the share was above levels of one year ago.

- Consumers’ planned spending on services over the next six months softened but remained healthy. The share who said “yes” fell, while those who said “maybe” and “no” increased. Consumer spending trends in 2026 remain focused on cheap thrills and necessary services – and away from expensive and highly discretionary activities.

“Consumers’ write-in responses on factors affecting the economy continued to skew towards pessimism. Comments about prices, inflation and the cost of goods remained at the top of consumer’s minds. Mentions of trade and politics also increased in February. Labor market mentions eased a bit, while observations about immigration increased somewhat,” Peterson says.

Consumer Income & Spending

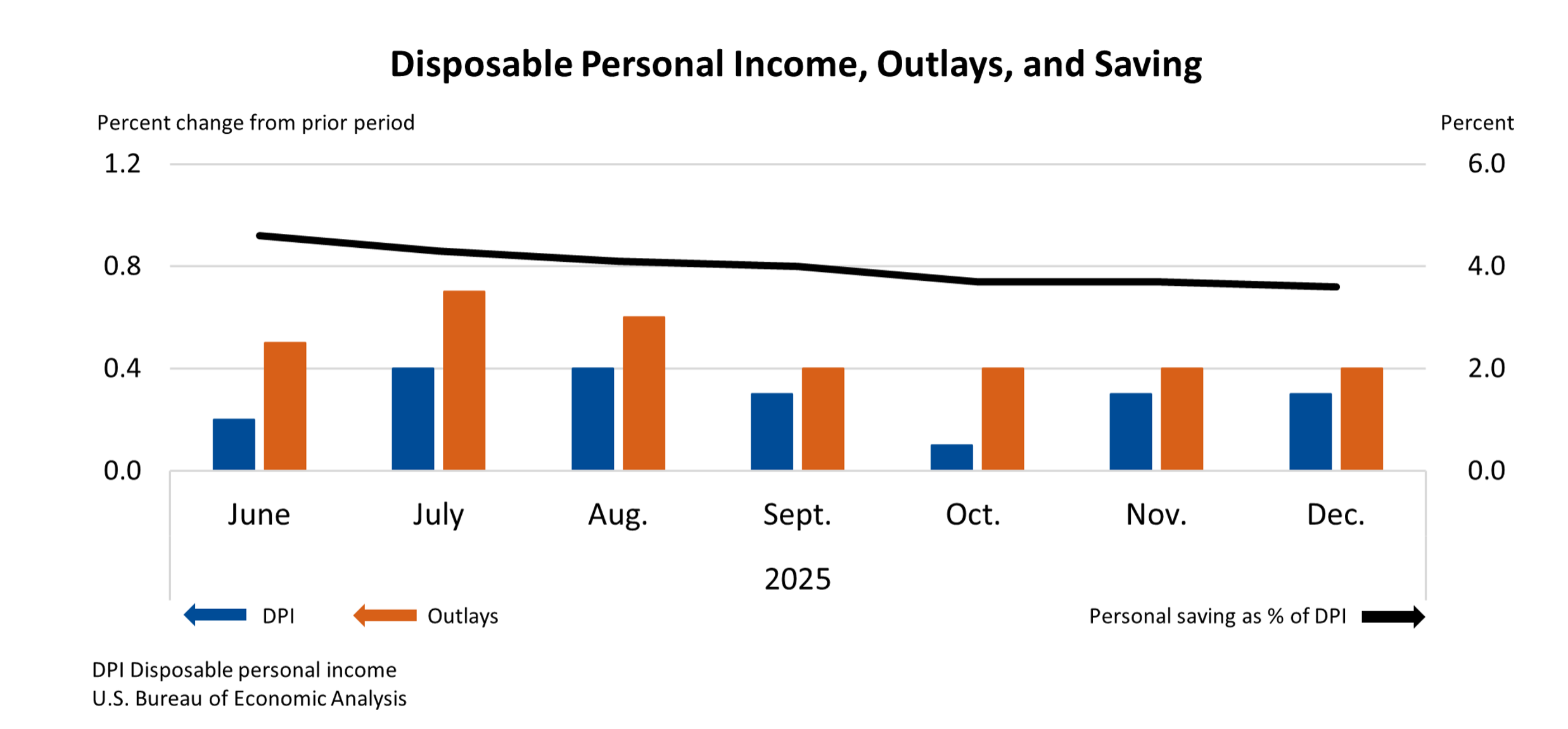

In December, personal income increased $86.2 billion (0.3% at a monthly rate), according to the U.S. Bureau of Economic Analysis (BEA). Disposable personal income (DPI) – personal income less personal current taxes – increased $75.7 billion (0.3%), while personal consumption expenditures (PCE) increased $91 billion (0.4%).

Personal outlays – the sum of PCE, personal interest payments and personal current transfer payments – increased $90.2 billion in December. Personal saving was $830.8 billion, and the personal saving rate, which is personal saving as a percentage of disposable personal income, registered 3.6%.

The $91 billion increase in current-dollar PCE reflected an increase of $98.5 billion in spending on services and a decrease of $7.5 billion in spending on goods.

Key takeaways, courtesy of the U.S. Bureau of Economic Analysis:

- In December, the PCE price index increased 0.4% month-over-month. Excluding food and energy, the PCE price index increased at the same rate.

- The PCE price index increased 2.9% year-over-year. Excluding food and energy, the PCE price index increased 3% from one year ago.