- KPI – December 2025: State of Business – Automotive Industry

- KPI – December 2025: State of Manufacturing

- KPI – December 2025: State of the Economy

- KPI – December 2025: Consumer Trends

- KPI – December 2025: Recent Vehicle Recalls

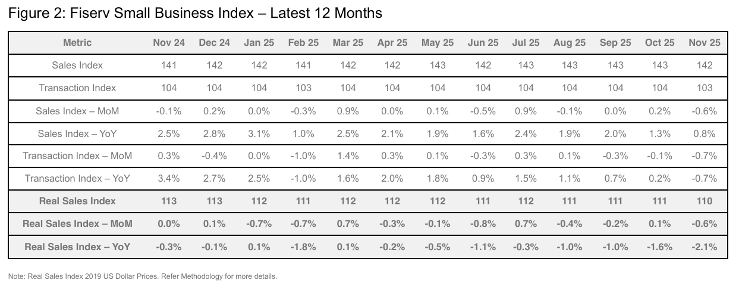

In November, the Fiserv Small Business Index was 142.3 – posting a year-over-year gain of 0.8% but a month-over-month decline of 0.6%. The Fiserv Small Business Transaction Index registered 103.3, with a year-over-year and month-over-month decrease of 0.7%. According to report analysis, these results indicate slight contraction in consumer activity compared to October, despite modest annual growth in sales.

Key takeaways, courtesy of the Fiserv Small Business Sales Index:

- Small business holiday performance showed solid early gains but lost momentum after a strong Black Friday. The pre-holiday period, including the week before Thanksgiving, posted steady growth for restaurants (2.9% and 3.6%, respectively) and core retail strength (3.9%), the latter of which helped to lift overall retail (1.9%). Black Friday maintained relatively high momentum for core retail (3.1%) and restaurants (2.9%). However, retail momentum slowed over the weekend, with Saturday down 2.1% and the full weekend simmered at minus-2.6%.

- Seasonally adjusted retail sales were down 1.1% year-over-year, despite a 1.1% jump in foot traffic. Growth was driven entirely by a significant decrease in average ticket size (minus-2.3%). Compared to October, sales were down 1.4%, also driven by lower foot traffic (minus-0.8%).

- Discretionary sales were muted at minus-0.1% year-over-year, while spending on essentials grew by 2.1%. Total goods sales declined 0.5% year-over-year, while services increased 1.4%.

- Despite facing extraordinary economic pressure, the small business sector continues to demonstrate perseverance. The NFIB Small Business Optimism Index registered 99.0 in November – up 0.8 points month-over-month. Of the 10 Optimism Index components, six increased, three decreased and one remained unchanged. An increase in those expecting real sales to be higher contributed most to the rise in the Optimism Index.

“Although optimism increased, small business owners are still frustrated by the lack of qualified workers. Despite this, more firms still plan to create new jobs in the near future,” says Bill Dunkelberg, NFIB chief economist.

Important takeaways, courtesy of NFIB:

- The net percentage of owners raising average selling prices rose 13 points to a net 34% (seasonally adjusted) – the highest reading since March 2023 and the largest monthly jump in the survey’s history.

- Twenty-one percent of small business owners cited labor quality as their single most important problem, down six points and erasing most of October’s sudden increase. Labor quality ranked as the top problem, six points ahead of inflation, which ranked second.

- The net percentage of owners expecting higher real sales volumes rose nine points to a net 15% (seasonally adjusted). This component contributed the most to the rise in the Optimism Index.

- The average rate paid on short maturity loans was 7.9% in November, down 0.8 points from October and the lowest level since May 2023.

- When asked to evaluate the overall health of their business, 11% reported it as excellent (down one point) and 53% reported it as good (up two points). Thirty percent reported the health of their business as fair (down three points) and 5% reported it as poor (up one point).

- Sixty-four percent of small business owners reported that supply chain disruptions were affecting their business to some degree, up four points month-over-month.

- The Uncertainty Index rose three points from October to 91. An increase in owners reporting uncertainty about capital expenditure plans over the next three to six months was the primary driver of the rise in the Uncertainty Index.

- The net percentage of owners expecting better business conditions fell five points to 15% (seasonally adjusted). Expectations for better business conditions fell 32 points since January.

Professionals in the automotive, RV and powersports industries remain steadfast in their efforts to evolve their business models and grow their brands in the face of adversity. As such, the monthly Key Performance Indicator Report serves as an objective wellness check on the overall health of our nation, from the state of manufacturing and vehicle sales to current economic conditions and consumer trends. Below are a few key data points explained in further detail throughout the report.

Key Data Points:

- In November, economic activity in the manufacturing sector contracted for the ninth consecutive month following a two-month expansion preceded by 26 straight months of contraction, according to the nation’s supply executives in the latest ISM Manufacturing PMI Report. The Manufacturing PMI registered 48.2%, a 0.5-percentage point decrease compared to a reading of 48.7% in October.

- The Global Light Vehicle (LV) selling rate remained strong at 95 million units per year. While the overall market dipped 2% year-over-year, year-to-date sales are up 4% with 83.6 million vehicles sold.

- According to the quarterly forecast prepared by ITR Economics for the RV Industry Association (RVIA), RV wholesale shipments are projected to increase slightly by year-end to 337,000 units, then see continued growth to the mid-300,000 unit range in 2026.

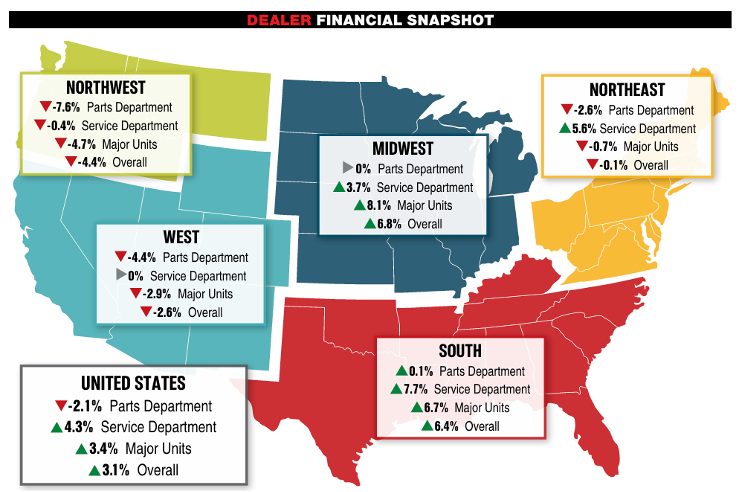

- Powersports Business says dealers across the country reported an overall combined revenue increase of 3.1% year-over-year in October, according to composite data from more than 1,700 dealerships in the U.S. that utilize CDK Lightspeed DMS. On average, dealerships were up 3.4% in major units and 4.3% in service, but down 2.1% in parts.