- KPI – December 2025: The Brief

- KPI – December 2025: State of Business – Automotive Industry

- KPI – December 2025: State of the Economy

- KPI – December 2025: Consumer Trends

- KPI – December 2025: Recent Vehicle Recalls

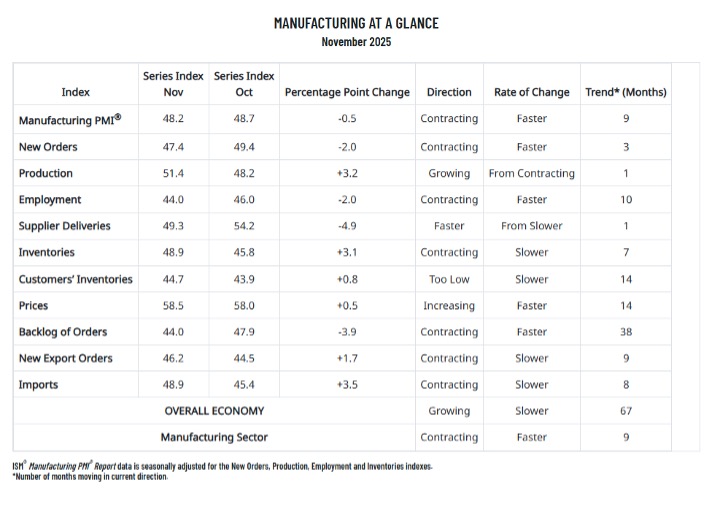

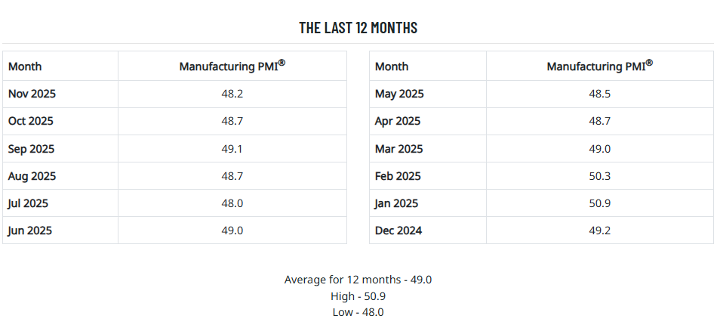

Economic activity in the manufacturing sector contracted in November for the ninth consecutive month, following a two-month expansion preceded by 26 straight months of contraction, according to the nation’s supply executives in the latest ISM Manufacturing PMI Report. The Manufacturing PMI registered 48.2% in November, a 0.5% decrease compared to the reading of 48.7% in October.

“In November, U.S. manufacturing activity contracted at a faster rate, with pullbacks in supplier deliveries, new orders, and employment leading to the 0.5-percentage point decrease of the Manufacturing PMI. Continuing a recent trend, a previous month’s improvement in one index was evident in another gauge. After new orders strengthened in August, production improved in September. An improvement in the Backlog of Orders Index in October transferred to the Production Index, which expanded in November (as backlogs pulled back). However, the New Orders and Employment indexes both dipped two percentage points, underscoring the ongoing economic uncertainty,” says Susan Spence, MBA, chair of the Institute for Supply Management (ISM) Manufacturing Business Survey Committee.

Data shows 58% of the sector’s gross domestic product (GDP) contracted in November. In addition, the percentage of GDP in strong contraction (registering a composite PMI of 45% or lower) decreased slightly, at 39% compared to 41% in October.

“The share of sector GDP with a PMI at or below 45% is a good metric to gauge overall manufacturing weakness. Of the six largest manufacturing industries, three (Computer & Electronic Products; Food, Beverage & Tobacco Products; and Machinery) expanded in November,” says Spence.

Important takeaways, courtesy of the Manufacturing ISM Report On Business:

- Decreases in two of the four demand indicators (Backlog of Orders and New Orders) “overwhelmed” the gains posted by the New Export Orders and Customers’ Inventories indexes. The Customers’ Inventories Index contracted at a slower rate. A “too low” status for the Customers’ Inventories Index is usually considered positive for future production.

- Output production jumped into expansion; however, employment contracted at a faster pace, as 67% of panelists indicated that managing headcounts is still the norm at their companies, as opposed to hiring.

- Inputs—defined as supplier deliveries, inventories, prices and imports—were mixed, with the Supplier Deliveries Index indicating faster deliveries, the Inventories Index contracting at a slower rate and the Prices Index continuing to reflect increases. The Imports Index contracted at a slower rate.

What Respondents Are Saying:

- “New order entries are within the forecast. We have increased requests from customers to get their orders sooner. Transit time on imports seems to be longer.” [Machinery]

- “We are starting to institute more permanent changes due to the tariff environment. This includes reduction of staff, new guidance to shareholders and development of additional offshore manufacturing that would have otherwise been for U.S. export.” [Transportation Equipment]

- “Tariffs and economic uncertainty continue to weigh on demand for adhesives and sealants, which are primarily used in building construction.” [Chemical Products]

- “No major changes at this time, but going into 2026, we expect to see big changes with cash flow and employee headcount. The company has sold off a big part of the business that generated free cash while offering voluntary severance packages to anyone.” [Petroleum & Coal Products]

- “Business conditions remain soft as a result of higher costs from tariffs, the government shutdown and increased global uncertainty.” [Miscellaneous Manufacturing]

- “The unstable market has made pricing fluctuate in a very volatile way. I have had to reduce suppliers for raw materials to maintain a better direct cost structure. Reducing my suppliers has reduced the availability of some items and created longer lead times.” [Fabricated Metal Products]

- “Business continues to be a struggle regarding long-term sourcing decisions based on tariffs and landing costs. External (or international) sourcing remains the lowest-cost solution compared to U.S. production/manufacturing. The delta is smaller now, reducing margins.” [Computer & Electronic Products]

- “The government shutdown has impacted our access to agricultural data, impacting agricultural markets and, as a result, decisions we make. Optimism for a tariff exemption on palm oil percolated but hasn’t come to fruition at this time.” [Food, Beverage & Tobacco Products]

- “Trade confusion. At any given point, trade with our international partners is clouded and difficult. Suppliers are finding more and more errors when attempting to export to the U.S.—before I even have the opportunity to import. Freight organizations are also having difficulties overseas, contending with changing regulations and uncertainty. Conditions are more trying than during the coronavirus pandemic in terms of supply chain uncertainty.” [Electrical Equipment, Appliances & Components]

- “Domestic and export business have been lackluster. Our customers are taking prompt orders only and still don’t have confidence to build inventory, much less make expansion plans. In fact, most of any kind of planning has been undermined by unpredictability due to inconsistent messaging from Washington. Artificial intelligence is in its infancy stages, producing confusing and, most often, inaccurate information. This also causes apprehensive consumer buying patterns, contributing to the challenge of forecasting demand.” [Wood Products]