- KPI – August 2025: The Brief

- KPI – August 2025: State of Manufacturing

- KPI – August 2025: State of the Economy

- KPI – August 2025: Consumer Trends

- KPI – August 2025: Recent Vehicle Recalls

Global Light Vehicle Sales

In July, the Global Light Vehicle (LV) selling rate improved to 94 million units per year. The market grew over 6% year-over-year, as sales reached 7.4 million units globally.

While trade tensions continue to shake the global outlook, monthly sales are holding steady. Data shows the auto market picked up in the U.S. market—posting a stronger selling rate in July despite OEM concerns. In addition, China “maintained its momentum” amid favorable price conditions and government support, according to reports. The Western European LV market improved approximately 4% year-over-year, as sales neared 1.1 million units last month.

“China, the U.S. and Europe made the largest contributions to year-over-year sales gains in July. As has been the case in previous months, Korea and South America also delivered solid increases, but Japan saw a decline for the first time since December 2024,” explains David Oakley, manager of Americas vehicle sales forecasts at GlobalData.

Next month, however, sales are expected to decrease 1.1% year-over-year. Although most regions will maintain stable volumes, Oakley says Europe and the Commonwealth of Independent States are both forecast to experience declines.

“Several European countries are struggling with low economic growth, while weak business and consumer confidence is affecting the light-vehicle market in France. The global selling rate is expected to reach 89.8 million units in August 2025, down slightly from a rate of 90.1 million units last year,” says Oakley, who is hopeful the trade war will shift tides.

“The U.S. has reached agreements with various trading partners, although some disputes remain, particularly with China and within North America,” he adds. “This slightly more favorable environment should support light-vehicle sales, and our full-year 2025 forecast now stands at 90.3 million units, representing growth of 1.7% year-over-year.”

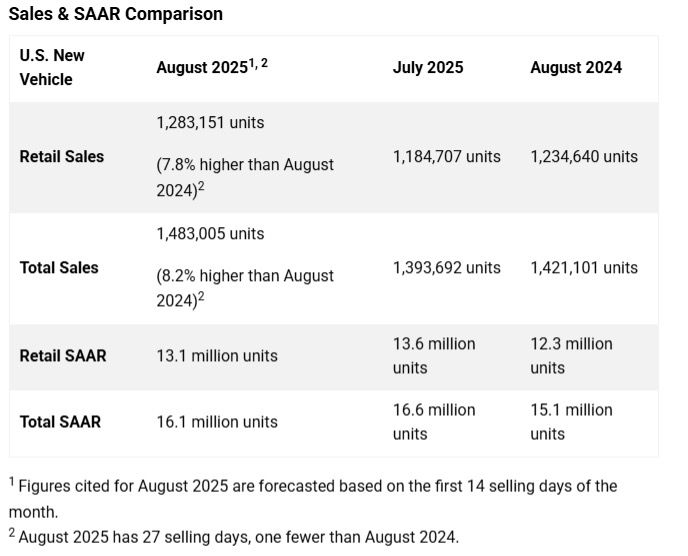

U.S. New Vehicle Market

Total new vehicle sales in August, including retail and non-retail transactions, are projected to hit 1,483,000—an 8.2% year-over-year increase, according to a joint forecast from J.D. Power and GlobalData.

“August new vehicle sales are expected to climb 8.2% from a year ago, including a 7.8% increase in retail volume. A strong result, although the results should be viewed in the context of several unusual factors that are distorting typical monthly sales trends,” says Thomas King, president of the data and analytics division at J.D. Power.

Federal credits on EVs are set to expire on September 30, encouraging many shoppers to accelerate future purchases. As a result, he says EV retail share in August is expected to reach an all-time high of 12%, compared with 9.5% a year ago.

In addition, Labor Day—typically one of the highest sales volume weekends of the year—lands in the August 2025 sales reporting period.

“This year, manufacturers have kept incentives restrained due to tariffs. Normally, incentives as a percentage of MSRP increase by about half a point from January through late summer, but this year they’ve slipped to 6.2% in August from 6.3% in January, underscoring the effect of tariff-related cost pressures,” King says.

He also points to lease returns at historically low levels, following the reduced leasing activity during the 2022 supply shortages. With fewer lease customers cycling back into the market, King says new vehicle sales are facing added pressure compared with typical seasonal patterns.

From a total sales perspective, fleet deliveries are expected to reach 199,854 units in August—up 11.2%. However, King notes the increase is skewed, primarily due to the low baseline recorded last year. Fleet volume is forecast to represent 13.5% of total light-vehicle sales, an increase of 0.4% year-over-year.

“In sum, August’s retail sales results point to solid new vehicle demand. The results are unquestionably inflated by shoppers accelerating their electric vehicle purchases to take advantage of Federal EV credits, but the sales pace for non-EVs remains robust, especially given the modest discounts available on those vehicles,” King says.

Key Takeaways, Courtesy of J.D. Power:

- Retail buyers are on pace to spend $54.6 billion on new vehicles, up $3.2 billion year-over-year.

- Internal combustion engine (ICE) vehicles are projected to account for 72.2% of new vehicle retail sales, a decrease of 5.6% from a year ago. Meanwhile, plug-in hybrid vehicles (PHEV), EVs and hybrid electric vehicles are expected to make up 2.5%, 12.8% and 12.6% of new vehicle retail sales.

- Trucks/SUVs are on pace to account for 82% of new vehicle retail sales, up 2.1%.

- Leasing is expected to account for 23% of sales, down 1.1% from a year ago.

- The average new vehicle retail transaction price is expected to reach $44,750, up $985 year-over-year.

- Average incentive spending per unit is expected to hit $3,105, up $38 year-over-year.

- Average monthly finance payments are on pace to hit $743, up $13 from a year ago. The average interest rate for new-vehicle loans is expected to be 6.4%, down 0.38%.

- Total retailer profit per unit, which includes vehicle gross plus finance and insurance income, is expected to be $2,202, down $7 year-over-year, but up $10 from July 2025. Total aggregate retailer profit from new-vehicle sales for this month is projected to be $2.7 billion, up 2.6% year-over-year.

“September sales will be influenced by multiple cross-currents,” King says. “With the federal EV tax credit expiring at the end of the month, automakers are expected to make a final, aggressive push to move remaining inventory. At the same time, tariffs are shaping pricing and incentive strategies, adding an average cost of $4,275 per vehicle, though the effect varies significantly by model. So far, manufacturers have managed to keep price hikes relatively restrained, with some vehicles unaffected. Further adjustments are likely as the year unfolds and new model-year introductions arrive, though many companies may hold back their most definitive incentive actions until year-end.”

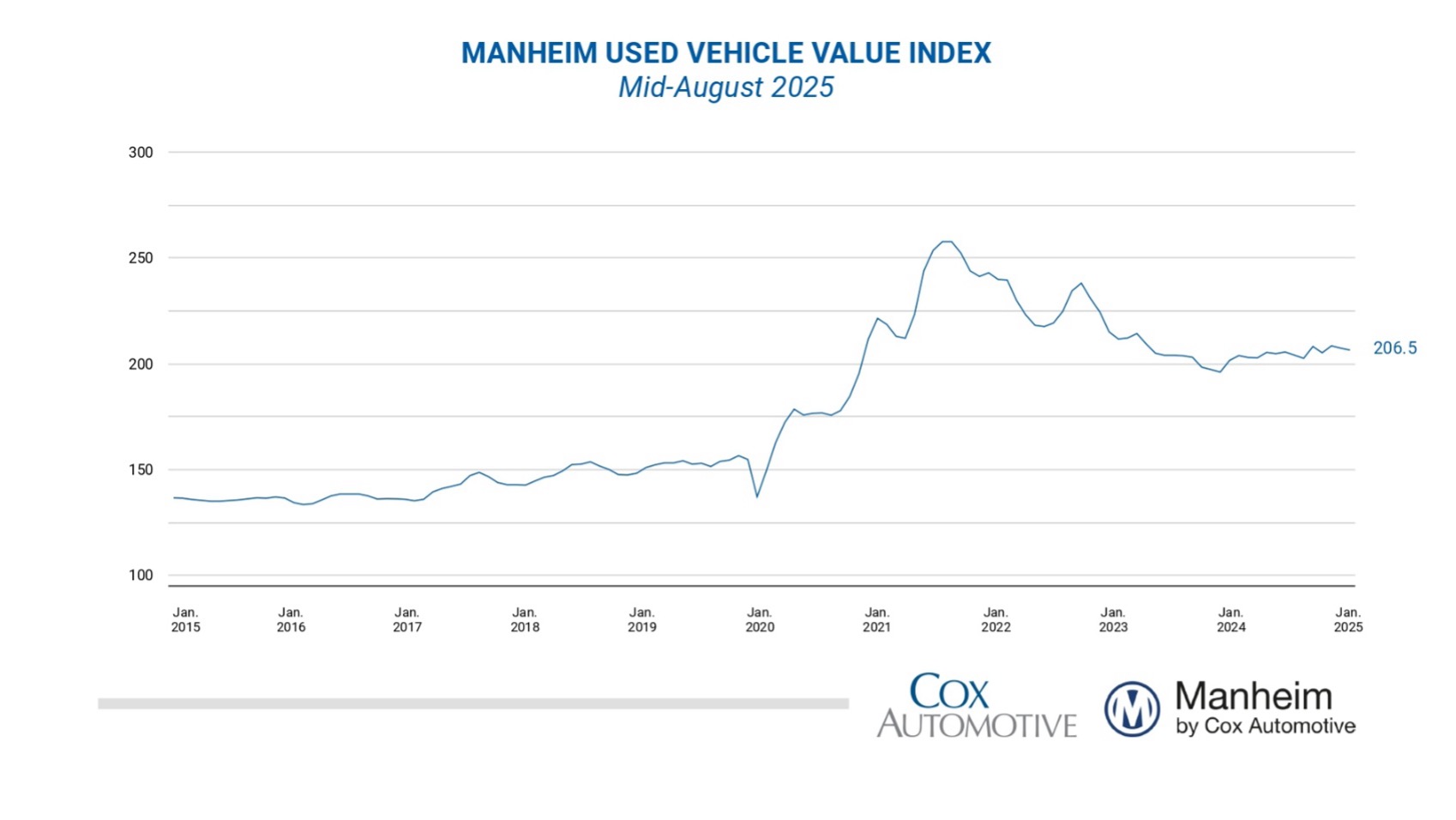

U.S. Used Market

Wholesale used-vehicle prices (on a mix-, mileage- and seasonally-adjusted basis) decreased from July during the first 15 days of August. The mid-month Manheim Used Vehicle Value Index dropped to 206.5, rising only 1.2% from the full month of August 2024.

“We started to see stronger sales trends in late July and early August for retail and wholesale markets, and that’s causing some additional volatility in wholesale pricing trends in recent weeks, against a stronger comparison from last year,” says Jeremy Robb, senior director of economic and industry insights at Cox Automotive. “In the first two weeks of August, non-seasonally adjusted prices are appreciating more than usual, though the seasonal adjustment was a bit stronger, causing the index to decline at the mid-month point.”

“Used retail supply has further tightened in recent weeks to the tightest level since early April, and that is keeping buyers active at Manheim to replenish inventory. While the tariffs induced much volatility in the automotive market earlier this year, we still see solid demand for both retail and wholesale vehicles,” he continues.

Vehicle segments posted mixed results as it relates to seasonally-adjusted prices on a year-over-year basis during the first half of August, according to Manheim. While the luxury and SUV segments were up 1.8% and 0.9%, respectively, trucks, midsize and compact cars were down 0.6%, 2% and 3.8% year-over-year. With federal tax credits on the chopping block, the EV segment pulled ahead—posting gains of 4.2%. Results also varied month-over-month, with compact and midsize cars, as well as EVs, up 0.9%, 0.7% and 0.5%, respectively. The SUV, truck and luxury segments declined 0.3%, 0.7% and 1.4% compared to the month prior.