- KPI – August 2025: The Brief

- KPI – August 2025: State of Manufacturing

- KPI – August 2025: State of Business – Automotive Industry

- KPI – August 2025: State of the Economy

- KPI – August 2025: Recent Vehicle Recalls

Below is a synopsis of consumer confidence, sentiment, demand and income/spending trends.

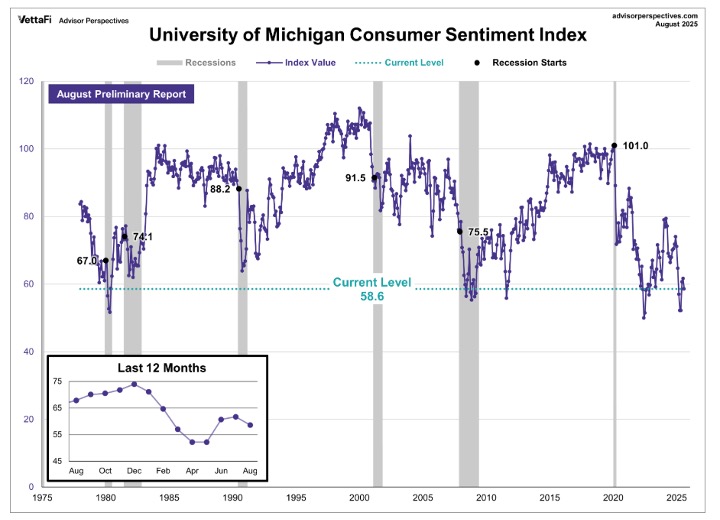

The University of Michigan Survey of Consumers—a survey consisting of approximately 50 core questions covering consumers’ assessments of their personal financial situation, buying attitudes and overall economic conditions—registered 61.7 in July and posted a preliminary reading of 58.6 in August, declining 5%.

“This deterioration largely stems from rising worries about inflation. Buying conditions for durables plunged 14% (its lowest reading in a year) on the basis of high prices. Current personal finances declined modestly amid growing concerns about purchasing power,” says Joanne Hsu, director of Surveys of Consumers. “In contrast, expected personal finances inched up a touch along with a slight firming in income expectations, which remain subdued.”

Overall, consumers are no longer bracing for the worst-case economic scenario, which was the fear when reciprocal tariffs were announced and then paused in the spring.

“However, consumers continue to expect both inflation and unemployment to deteriorate in the future,” Hsu adds.

- Year-ahead inflation expectations rose from 4.5% last month to 4.9% this month—up across multiple demographic groups and all three political affiliations.

- Long-run inflation expectations increased from 3.4% in July to 3.9% in August. This month ended two consecutive months of receding inflation for short-run expectations and three straight months for long-run expectations.

“Still, both readings remain well below the highs seen briefly in April and May 2025,” Hsu clarifies.

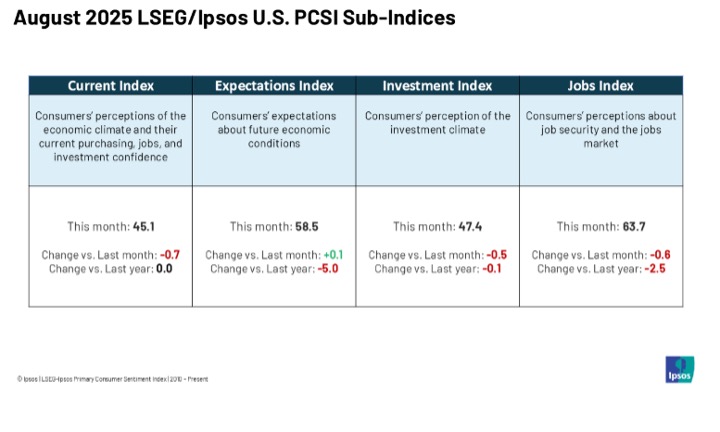

Caption: The LSEG/Ipsos Primary Consumer Sentiment Index for August 2025 is at 53.4. Fielded from July 25-29, 2025*, the Index is stable (-0.4 points) from last month.

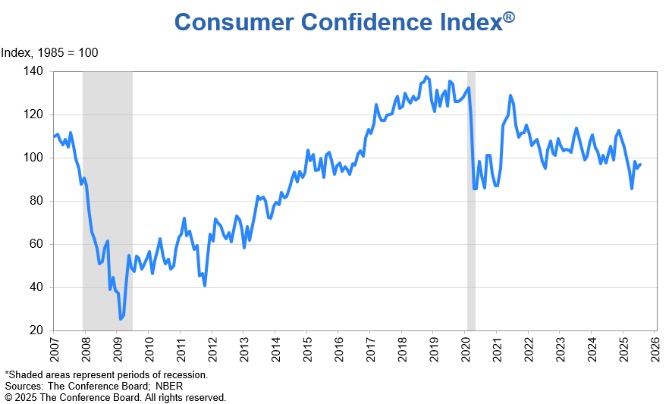

In addition, The Conference Board Consumer Confidence Index improved by two points from 95.2 in June (revised up by 2.2 points) to 97.2 (1985=100) in July. The Present Situation Index—based on consumers’ assessment of current business and labor market conditions—fell 1.5 points to 131.5. Meanwhile, the Expectations Index—based on consumers’ short-term outlook for income, business and labor market conditions—rose 4.5 points to 74.4. Overall, expectations remained below the threshold of 80, which historically signals a recession ahead.

“Consumer confidence has stabilized since May, rebounding from April’s plunge, but remains below last year’s heady levels,” says Stephanie Guichard, senior economist of global indicators at The Conference Board. “In July, pessimism about the future receded somewhat, leading to a slight improvement in overall confidence.”

For example, she says all three components of the Expectation Index improved, with consumers feeling “less pessimistic” about future business conditions and employment—and more optimistic about future income.

Consumers’ assessment of the present situation was little changed. While they were slightly more positive about current business conditions in July, their appraisal of current job availability weakened for the seventh consecutive month, reaching its lowest level since March 2021.

“Notably, 18.9% of consumers indicated that jobs were hard to get in July, up from 14.5% in January,” Guichard says.

Data shows the modest gain in confidence was driven by consumers over 35 years old and shared across all income groups, except those earning the least (with household annual income below $15K). By partisan affiliation, confidence improved in July among Republican consumers and was stable for Democrats and Independents.

Key Takeaways, Courtesy of The Conference Board:

- Consumers’ outlook on stock prices continued to recover from April’s 16-month low, with 47.9% expecting stock prices to increase over the next 12 months, up from 37.6% three months ago.

- The share of consumers expecting interest rates to rise declined to 53%. More consumers expected interest rates to fall (21.2% vs. 18.4% in June). A special question asking consumers about the direction of various interest rates suggested that they largely believe mortgage rates, auto loan rates and credit card rates were more likely to rise than other types of interest rates. Specifically, consumers anticipated credit card rates to jump the most.

- Consumers’ views of their Current and Future Family’s Financial Situation remained solid overall, albeit a slight deterioration occurred in July.

- The share of consumers expecting a recession over the next 12 months rose slightly but remains above 2024 levels.

- In July, purchasing plans for cars and homes declined but remained stable on a 6-month moving average basis. Consumers’ plans for purchasing big-ticket items were mixed, especially for appliances, while plans to buy most electronic goods ticked up slightly. Consumers’ intentions to purchase more services weakened for a second month, with almost all service categories declining. Dining out remained number one among spending intentions in services. However, dining out was also one of the categories to post the largest decline in spending intentions in July, along with transportation and lodging related to personal travel. Consistent with these findings, vacation intentions were down as well. Slightly more consumers planned to travel abroad, while intentions to travel in the U.S. declined.

According to Guichard, consumers’ write-in responses showed tariffs are top of mind—more specifically, their impact on prices in the coming months. In addition, references to high prices and inflation rose in July, even though consumers’ average 12-month inflation expectations eased to 5.8%, down from 5.9% in June and a peak of 7% in April.

“A number of survey respondents mentioned the recent budget reconciliation legislation passed by Congress (referring to it as the “Big Beautiful Bill”), with some consumers praising its potential positive economic impact and others expressing concerns,” she says. “However, the bill and its implications were relatively low on the list of themes that consumers were focused on in July.”

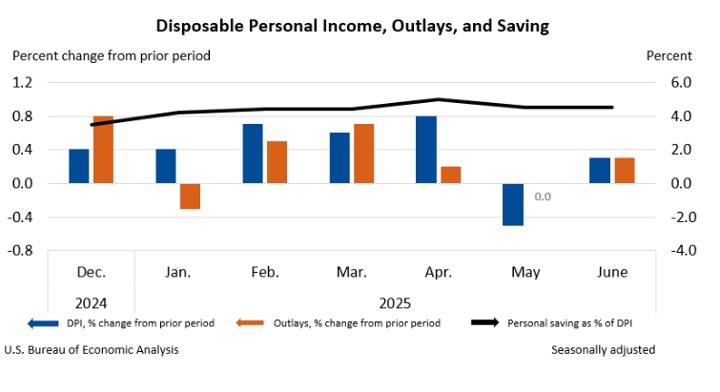

Consumer Income & Spending

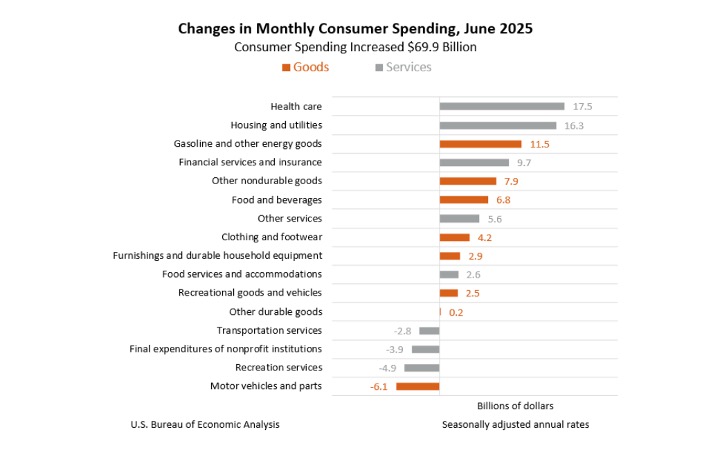

According to the U.S. Bureau of Economic Analysis (BEA), in June personal income increased $71.4 billion (0.3% at a monthly rate), while disposable personal income (DPI)—personal income less personal current taxes—increased $61 billion (0.3%) and personal consumption expenditures (PCE) increased $69.9 billion (0.3%).

Personal outlays—the sum of PCE, personal interest payments and personal current transfer payments—increased $69.5 billion. Personal saving was $1.01 trillion, and the personal saving rate—personal saving as a percentage of disposable personal income—registered 4.5%.

Important Takeaways, Courtesy of BEA:

- In June, the $69.9 billion increase in current-dollar PCE reflected increases of $40.1 billion in spending on services and $29.9 billion in spending on goods.

- Compared to the preceding month, the PCE price index increased 0.3%. Excluding food and energy, the PCE price index also increased 0.3%.

- The PCE price index increased 2.6% year-over-year. Excluding food and energy, the PCE price index increased 2.8% from one year ago.